-

Advisers believe Consumer Duty will change the way they think about overall consumer cost

-

But they also believe that the impact of the Duty could exacerbate the advice gap

-

Advisers are confident they can identify vulnerability, but are still underestimating the extent

Still work to do on Consumer Duty and Vulnerable Customers

Advisers say Consumer Duty will be good for clients, if you are still a client!

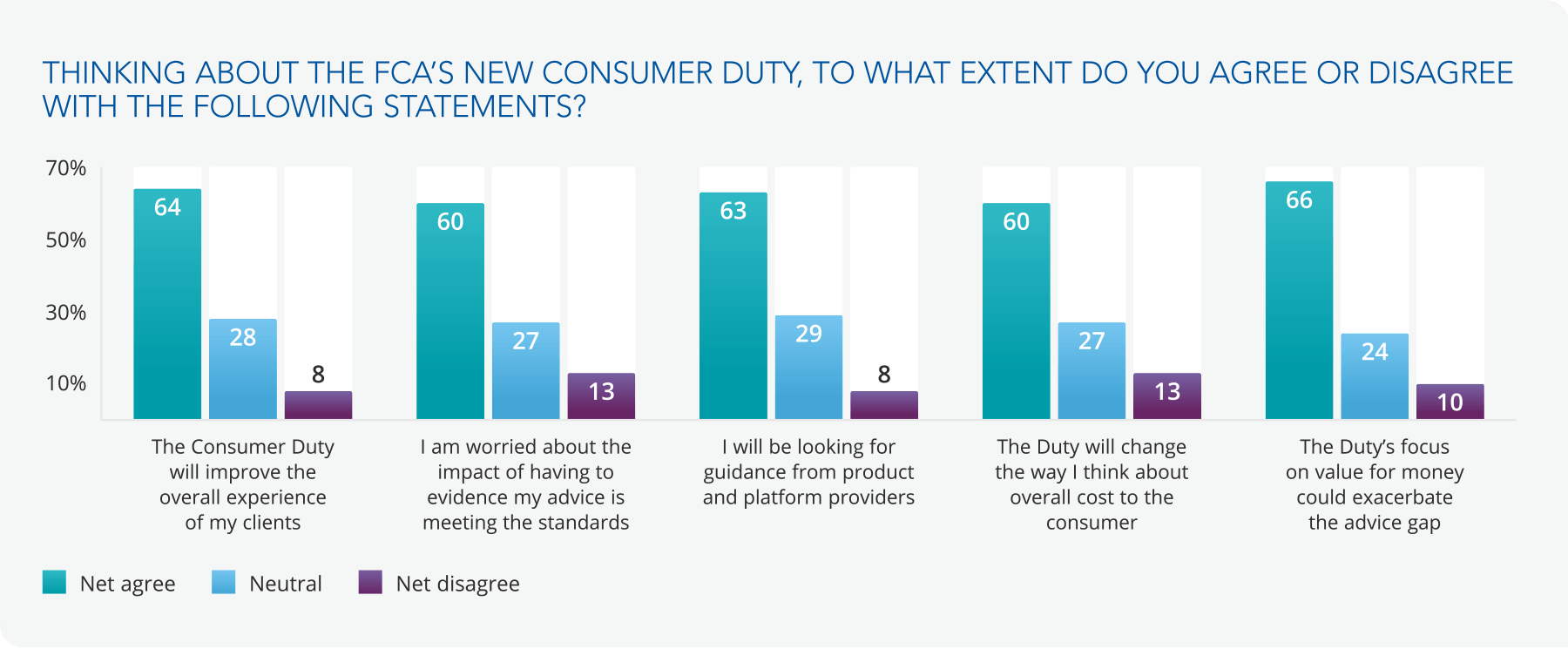

Our Barometer suggests advisers have mostly bought into the vision of the Consumer Duty, if not entirely comfortable with the nuts and bolts of how it will work in practice: a 64% majority of advisers believe it will improve the client experience, but a similar 60% majority are worried about the impact of having to evidence that they are delivering good client outcomes. It follows then that 63% of advisers would be looking for help with compliance from product and platform providers; the latter have a clear opportunity to strengthen their relationships by assisting advisers.

The fact that 60% of advisers agree that the Duty will change the way they think about overall cost (and value) to the consumer is confirmation that the Duty is having the FCA’s desired effect. As the client-facing part of the distribution chain, advisers have to consider not only their own fees but all charges in the chain.

The unintended consequence of this is that 66% of advisers believe that the Duty’s focus on value for money will mean marginal clients may go unserved and drop into the advice gap. The better economies of scale enabled by robo-advice models could be part of the answer in serving these consumers. Nevertheless, if there is a growing segment of investors seeking advice that cannot access it, in part due to the impact of the Duty, this would be a worrying development for the FCA.

Advisers are more confident on VC strategies, but they are still underestimating the true numbers

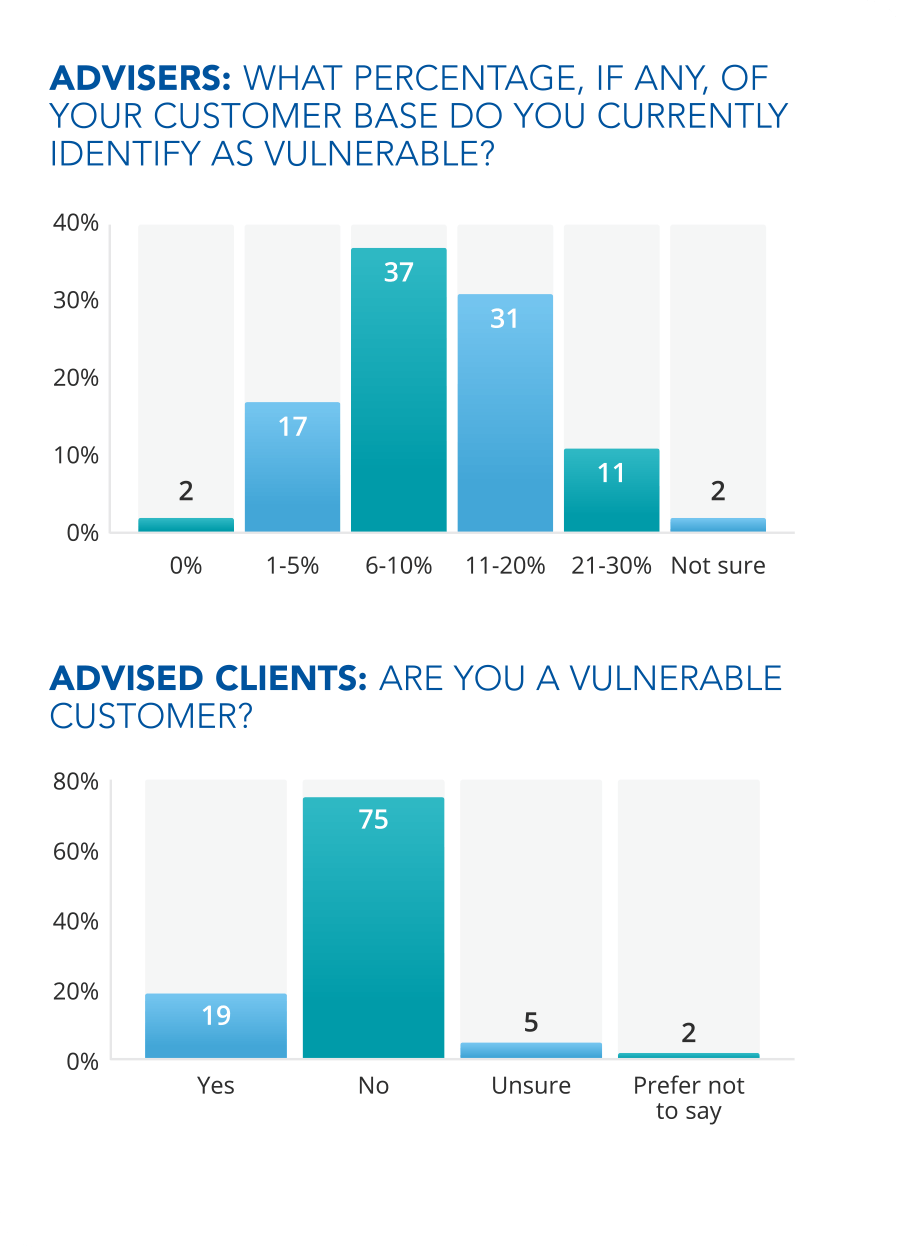

An impressive 86% of advisers are confident their firms have a strategy in place to identify vulnerable customers (up from 72% last time). Most advisers estimate between 6% and 20% of their customers as vulnerable, with the average being 11.5% – this is consistent across age groups, geographies, and assets.

How does this compare to how advised clients identify themselves, however? Amid a cost-of-living crisis, with ongoing impacts from covid and new ways of working, 19% of the advised clients we surveyed currently identify as vulnerable. This is a big increase from the 12% figure in our last survey.

When we dig into the advised client data, it reveals some interesting findings that may go against ingrained thinking. Younger clients were more likely to identify as vulnerable. Over 20% of 35-44 and 45-54 cohorts identified as vulnerable. This compares to only 6% and 7% for the 55-65 and 65-70 cohorts. The non-advised investor data showed a similar pattern (10% of 35-44 and 16% of 45-54 identified as vulnerable but only 6% of 55-64 and 8% of 65-70).

This large gap could be explained by a greater reluctance on the part of older generations to admit they are vulnerable. If that is the case, the real extent of vulnerability could be greater than these numbers imply. This finding also emphasises how critical it is that financial firms have systems in place to flag potential vulnerability in their client interactions.

“That the Duty will change the way many advisers think about the total cost to the consumer is a big positive on the face of it. However, the fact that advisers believe the focus on value for money could worsen the advice gap should be a serious concern for the FCA. These two findings highlight the intended and unintended effects that policies can have.

The industry may still be under-estimating the true extent of client vulnerability. The current economic, geo-political and social conditions may be acting as a trigger for heightened levels

of vulnerability. Discouragingly, that view looks to be backed up by the latest UK stats that show those on long-term sickness hit a record high of 2.5m in summer 2022.* Advisers may need to review their VC strategies to give greater weight to these factors.”

Andrew Phipps

Product Marketing Manager, Embark Group

* Source: Office of National Statistics, www.ons.gov.uk

Audio

Key Insight 1

Why are advisers more bullish than investors?

Why are advisers more bullish than investors?

Key Insight 2

Search for scale: is another M&A wave coming?

Search for scale: is another M&A wave coming?

Key Insight 3

What impact will the cost of living have on savings?

What impact will the cost of living have on savings?

Key Insight 4

Could Consumer Duty exacerbate the advice gap?

Could Consumer Duty exacerbate the advice gap?

Focus On…

How often do your clients check their portfolios?

How often do your clients check their portfolios?

Download the full guide

Looking to download the full Embark Investor Confidence Barometer? Simply click the button and download the guide.

Get in touch

If you have any questions or wish to find out more about the Embark Investor Confidence Barometer, please contact us here.