-

Advisers see industry consolidation as a positive for advice firms and clients

-

Rising costs and regulations mean small firms see the inevitable need for scale

-

Industry-wide quest for scale may begin to address consumers in the advice gap

The rise of the networks: M&A in the Advice Industry

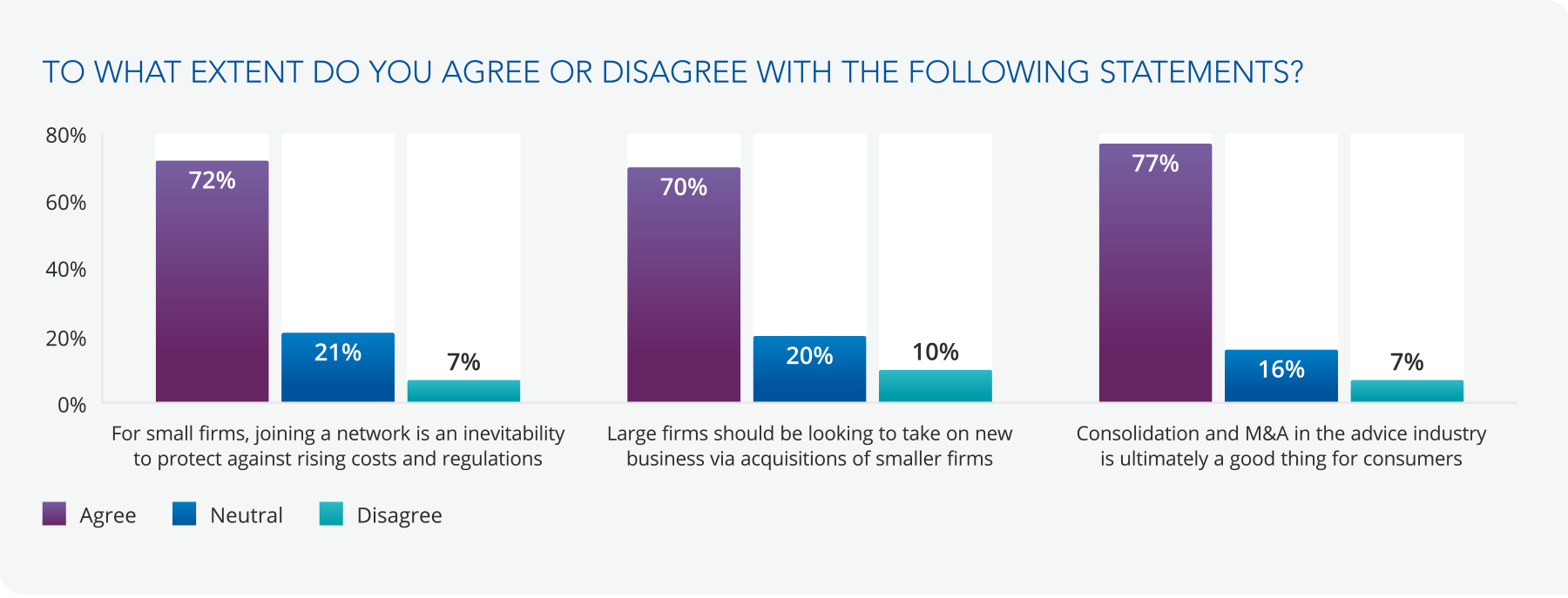

Bigger is better

Our survey paints a picture of a search for scale against a backdrop of tough competition, rising costs and the onerous impact of regulatory compliance. 72% of advisers believe that joining a network is now inevitable for small firms to protect against rising costs and regulations. Notably, the strongest agreement came from the firms with the fewest assets; 87.5% of adviser firms with assets under administration (AuA) under £500K. This strongly suggests the smallest firms know themselves that the conditions are against them if they cannot achieve critical mass fast.

Most advisers (70%) also believe that large firms should be looking to grow via acquisitions of smaller firms. Here, we saw the strongest agreement (92%) in the £400m-£500m AuA range – the very firms that might be doing the buying. Meanwhile, smaller firms who would most likely be the target of that buying (in the £500K-£10m AuA range) had the weakest agreement (64%). Overall, we see a picture of advisers everywhere admitting that scale is a ‘must have’ in the advice industry.

The strongest result on M&A was the 77% of advisers who agreed that consolidation in the advice industry is ultimately a good thing for consumers. This chimes with our findings on Consumer Duty, which advisers also believe will be a good thing for consumers. But compliance costs money due to the new processes required to evidence good outcomes and value for money. Joining a network that provides a greater level of centralised resource in these areas is seen to be a good thing for clients as well as advisers, if it makes ‘good customer outcomes’ more likely.

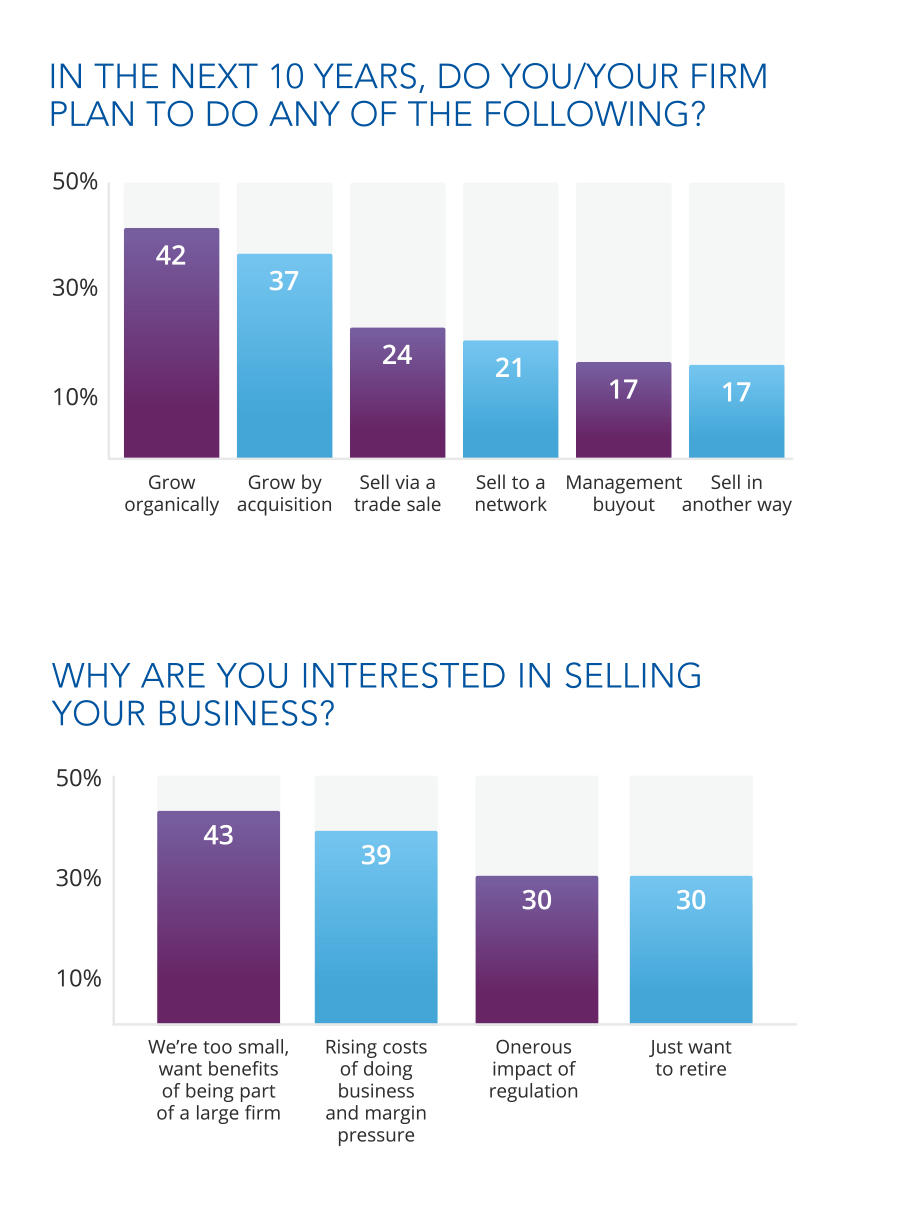

Grow or sell!

The need for scale is having a clear impact on business strategy. We see a picture of growth by any means, with a notable part of the industry prepared to sell their business if they cannot achieve the critical mass required to go it alone. Asked about their business plans for the next ten years, the most popular strategy among advisers surveyed was to grow organically (42%), followed closely by growth by acquisition (37%). On the other hand, around 1 in 5 adviser firms are prepared to sell, with trade sales and selling to a network being the leading options.

Of those advisers who are interested in selling, the need for scale comes out top again; the most popular reason (43%) was ‘we’re too small and we want the benefits of being part of a large firm’. The second but related reason was ‘the rising costs of doing business and margin pressure’.

This ‘achieve growth or sell’ trend describes and cements the rise of the large networks, which can take advantage of the economies of scale provided by larger AUAs, greater spending power and centralised costs. Advisers are also drawn by the opportunity to access exclusive centralised investment propositions, with model portfolios that can be tailored to clients alongside packaged risk profiling and cashflow tools.

The shared costs and resources a network provides means that advisers who join may be able to target a greater amount of clients under the Consumer Duty’s value for money focus than they could otherwise do as a standalone small firm. In this way, the industry’s accelerated search for scale could be a sensible response to higher regulatory burdens and a positive development for consumers in the advice gap.

“The need for scale comes out strongly in our survey. Indeed, the cost of regulatory compliance is making scale and delivering good client outcomes increasingly interlinked. Combined with tighter financial conditions and falling asset values, it could trigger a further wave of M&A in the financial planning industry as vulnerable firms are swallowed up opportunistically by the strong.

We are likely to see further horizontal integration of smaller advice firms into networks. Vertical integrations have also become more prominent, as large advisers and networks explore white labelling platform services and acting directly as a platform service provider. Of course, this will radically change the risk profile of adviser firms adding new regulatory and capital requirements.

White-labelling of platform technology and the centralised investment proposition can be a smart solution for medium-to-large, fast-growing adviser firms since it provides access to robust infrastructure and capability at a fraction of the time, cost, and risk associated with developing and running their own platform kit and investment products from the ground up.”

Jonathan Sandell

Group Head of Propositions, Embark Group

Audio

Key Insight 1

Why are advisers more bullish than investors?

Why are advisers more bullish than investors?

Key Insight 2

Search for scale: is another M&A wave coming?

Search for scale: is another M&A wave coming?

Key Insight 3

What impact will the cost of living have on savings?

What impact will the cost of living have on savings?

Key Insight 4

Could Consumer Duty exacerbate the advice gap?

Could Consumer Duty exacerbate the advice gap?

Focus On…

How often do your clients check their portfolios?

How often do your clients check their portfolios?

Download the full guide

Looking to download the full Embark Investor Confidence Barometer? Simply click the button and download the guide.

Get in touch

If you have any questions or wish to find out more about the Embark Investor Confidence Barometer, please contact us here.