“Some adviser firms have not yet updated their investment strategies for decumulation clients. In addition, they may not have adequately considered decumulation risks” FCA Sector Views 2019

“This concern appears to be borne out by research in recent months which also suggests that many firms are using the same investment strategy for decumulation clients as they do for accumulation clients. This is despite the different dynamics of clients’ needs in retirement and different risks, in particular sequence of returns risk and pound cost ravaging. Simply adopting the same investment strategy in retirement can be dangerous for clients and the FCA is on to this.” Rory Percival, Former FCA regulator

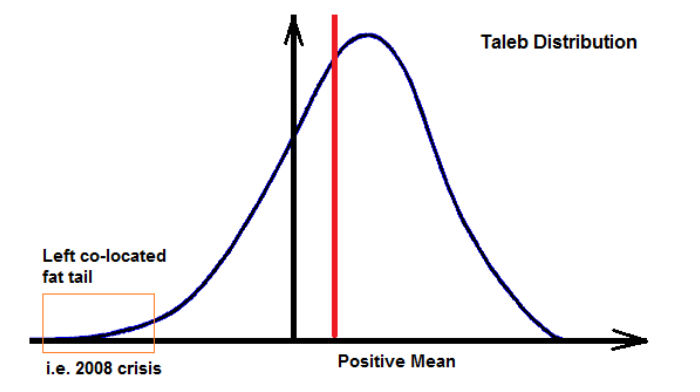

The expected return of a typical investment strategy has a distribution which normally provides a positive return over time but also carries a small but significant risk of suffering a big loss known as a ‘left tail’ event. This is known as a Taleb distribution, after Nassim Taleb of ‘Black Swan’ fame, and looks something like this:

Suffering from the kind of large investment loss represented by the left tail is never welcome, but in the accumulation phase, particularly through pound cost averaging if continuing to regularly invest at lower prices, diversified portfolios have historically recovered.

When in the decumulation or drawdown phase, however, this is not the case. The outcome for pension income here can be catastrophic, particularly for retirees just starting drawdown when a pension pot may be at its greatest and investment losses are crystalised immediately prior to or just after retirement. Even if not occurring at the outset, the impact of a left tail event and reverse pound cost averaging (so-called “pound cost ravaging” where a fixed withdrawal is being taken from a falling asset value) can be significant.

What can be done to stop these left tails wagging the pension income dog?

Several mitigants have been proposed and researched, including:

- Using options to provide ‘tail protection’. This is feasible in theory but is likely too complex and expensive to be practical for most individuals.

- Scenario analysis and stress testing. Various tools are available and, though they cannot foresee events, they can emphasise various outcomes and what a client may stand to lose. In practice these generally operate more as education than mitigation.

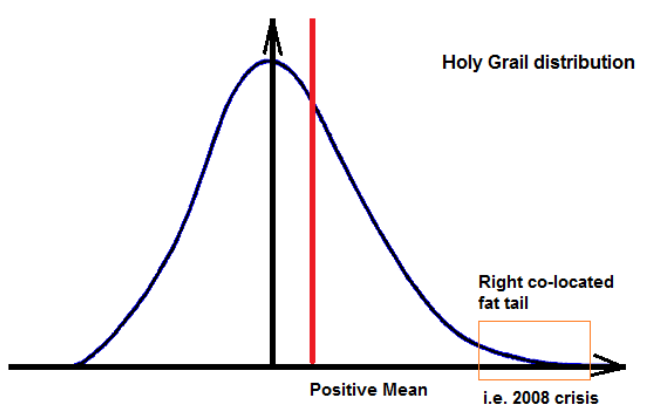

- Implement a complementary investment strategy that helps reduce the impact of market performance shocks. This is known as a holy grail distribution and looks something like this:

In 2008, certain strategies, notably ‘trend following’ systematic strategies, performed very well to help extend the right tail of return distributions for those who had adopted them.

Professor Clare and colleagues, based at Cass Business School, have extensively researched the impact of sequence risk in decumulation They have published their research in multiple papers and have reached one very definitive conclusion, having considered over 100 years of equity and bond return data:

By systematically switching equity exposure to cash when markets turn lower (and vice versa), according to an entirely rules-based strategy based on a trend following, sequence risk can be effectively mitigated.

The result of employing this strategy is that it reduces and shortens the left tail, resulting in higher sustainable withdrawal amounts each year when in decumulation.

Read more articles like this on our insights page

About the author

Geoff Brooks, CEO, Alpha Beta Partners

Geoff has over 30 years’ experience in strategic and leadership roles in major financial institutions in Europe, Asia and the USA; Geoff developed his career as a retirement and investment expert advising and developing drawdown and retirement solutions. His early career started with 4 major life companies NPI, Standard Life, Prudential and Friends Provident. Later to be appointed Head of Retirement for HSBC launching Stakeholder Pensions, DC solutions and drawdown. At the forefront of consumer rights and value for money Geoff led the HSBC customers to contract back into SERPS as the first Life company to do so.

The AB Lifetime portfolio, a diverse, mixed asset growth portfolio has licensed the Professors’ strategy to provide clients with a differentiated investment option for those in and entering the decumulation phase.

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on treated as a substitute for specific advice of any kind.

We make no warranties, representatives or undertakings about any of the content of this website (including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representation warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Geoff Brooks, CEO, Alpha Beta Partners

Geoff has over 30 years' experience in strategic and leadership roles in major financial institutions in Europe, Asia and the USA; Geoff developed his career as a retirement and investment expert advising and developing drawdown and retirement solutions. His early career started with four major life companies NPI, Standard Life, Prudential and Friends Provident. At the forefront of consumer rights and value for money, Geoff led the HSBC customers to contract back into SERPS as the first Life company to do so. Geoff is now playing a leading role in Alpha Beta Partners, a disruptive asset manager bringing retirement expertise and championing value for money and consumer outcomes.

Read more articles by this author

Be the first to hear news and insights from Embark Group

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.