Is the U.S. economy experiencing a soft patch, or is a recession on the horizon? Regardless of the outcome, history suggests that equities will continue to move higher in the coming months with an uptick in volatility.

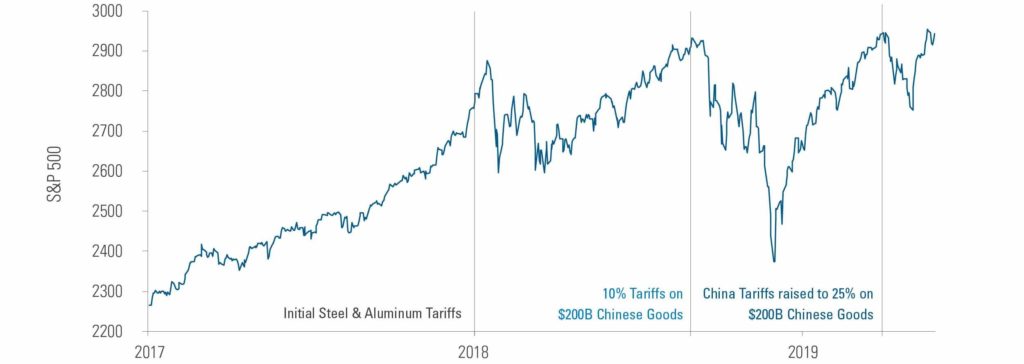

U.S. equities, as measured by the S&P 500, finished the first six months of 2019 up 18.5%, their best performance since 1997. While we still expect higher returns in the second half, several of the perceived positives that have driven equities to all-time highs may be less supportive going forward. Despite the U.S.-China trade détente that emerged from the G-20 summit in Japan, if an agreement can’t be forged in the coming months and tensions re-escalate, it could push equities lower like previous episodes when stocks sold off swiftly due to trade war fears. In our view, the recent trade “truce” could be a “sell the news” type of event due to the lack of substance and tangible progress (Exhibit 1).

Exhibit 1: Trade Escalations Have Come at Market Highs

S&P 500 price index: 12/30/16 – 6/28/19

Source: Factset, as of 6/28/19. Past performance is no guarantee of future results. Indexes are unmanaged, and not available for direct investment. Index returns do not include fees or sales charges. This information is provided for illustrative purposes only and does not reflect the performance of an actual investment.

The second perceived positive for stocks that could warrant a more cautious stance is the expected easing of Federal Reserve (Fed) policy. The markets are currently pricing in at least two interest rate cuts this year. Historically, Fed cuts are bearish for equities and the economy. Ten of the last 13 interest-rate hike cycles have ended with a recession because the Fed acted too late and lower rates couldn’t prevent the economy from rolling over.

Importantly, the current yield curve inversion has not persisted for a long time and it's relatively shallow, meaning there is still a chance the Fed can reverse course and manage a “soft landing” à la 1995 or 1998. Bull and bear markets are primarily a function of liquidity in the system. We think there's ample liquidity right now, and that should continue as rates head marginally lower and inflation remains contained. For now, we would view expected rate cuts as limited and more of an “insurance policy” to sustain growth.

Finally, the overall signal for the ClearBridge Recession Risk Dashboard has recently turned yellow from green, signalling caution. It’s important to note that a yellow signal does not mean that the market or economic cycle is over just quite yet. On average, the ClearBridge Recession Risk dashboard would be expected to turn yellow before both a recession and a market top. Additionally, the dashboard would have shown three yellow signals in the past that never worsened to red: 1995, 1998 and 2015.1 Although the economy avoided a recession in each of these instances, economic activity slowed substantially before quickly reversing course. Should the dashboard continue to erode and turn red, we would become much more cautious, given its much stronger recessionary track record. As a result, the U.S. economy is at a crossroads: soft patch versus recession on the horizon. Regardless of the outcome, history would suggest that equities will continue to move higher in the coming months, accompanied by an uptick in volatility.

In terms of positioning in this environment, we want to tread lightly in areas most at risk from both a trade perspective and a slowdown in global growth. Take technology, for example. The hardware side has a lot of exposure in China, and areas like semiconductors have been badly hit. Software, meanwhile, is much less affected by what's going on in China. Though the market may come down or tech may come under pressure, software is an area to maintain or even expand through volatility.

In the 10th year of a bull market, there are not a lot of stocks that offer both reasonable valuations and solid fundamentals. What does look attractive is a little controversial, like the pharmaceutical and biotechnology sub-sectors of health care, which continue to deal with pricing pressure and rhetoric over changes to the overall health care system.

Another sector where we see opportunity is energy pipelines. Energy companies are dealing with questions about global demand and how that will impact commodity prices. But as long as prices stay within a certain range, pipeline companies can thrive. After suffering through a multi-year bear market, in our view they offer attractive yields at moderate valuations.

1 The ClearBridge Recession Risk Dashboard was created in January 2016. References to the signals it would have sent in the years prior to January 2016 are based on how the underlying data was reflected in the component indicators at the time.

Investment risks:

Yields and dividends represent past performance and there is no guarantee they will continue to be paid.

Definitions:

The S&P 500 Index is an unmanaged index of 500 stocks that is generally representative of the performance of larger companies in the U.S.

The Federal Reserve Board ("Fed") is responsible for the formulation of U.S. policies designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments.

The Group of Twenty (also known as the G-20 or G20) is an international forum for the governments and central bank governors from 20 major economies. The members include 19 individual countries—Argentina, Australia, Brazil, Canada, China, France, Germany, India, Indonesia, Italy, Japan, Mexico, Russia, Saudi Arabia, South Africa, South Korea, Turkey, the United Kingdom and the United States—along with the European Union (EU). The EU is represented by the European Commission and by the European Central Bank.

The yield curve is the graphical depiction of the relationship between the yield on bonds of the same credit quality but different maturities.

Inverted yield curve refers to a market condition when yields for longer-maturity bonds have yields which are lower than shorter-maturity issues.

Forecasts are inherently limited and should not be relied upon as indicators of actual or future performance.

Important Information

All investments involve risk, including possible loss of principal.

The value of investments and the income from them can go down as well as up and investors may not get back the amounts originally invested, and can be affected by changes in interest rates, in exchange rates, general market conditions, political, social and economic developments and other variable factors. Investment involves risks including but not limited to, possible delays in payments and loss of income or capital. Neither Legg Mason nor any of its affiliates guarantees any rate of return or the return of capital invested.

Equity securities are subject to price fluctuation and possible loss of principal. Fixed-income securities involve interest rate, credit, inflation and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed income securities falls.

International investments are subject to special risks including currency fluctuations, social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Commodities and currencies contain heightened risk that include market, political, regulatory, and natural conditions and may not be suitable for all investors.

Past performance is no guarantee of future results. Please note that an investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

The opinions and views expressed herein are not intended to be relied upon as a prediction or forecast of actual future events or performance, guarantee of future results, recommendations or advice. Statements made in this material are not intended as buy or sell recommendations of any securities. Forward-looking statements are subject to uncertainties that could cause actual developments and results to differ materially from the expectations expressed. This information has been prepared from sources believed reliable but the accuracy and completeness of the information cannot be guaranteed. Information and opinions expressed by either Legg Mason or its affiliates are current as at the date indicated, are subject to change without notice, and do not take into account the particular investment objectives, financial situation or needs of individual investors.

The information in this material is confidential and proprietary and may not be used other than by the intended user. Neither Legg Mason or its affiliates or any of their officer or employee of Legg Mason accepts any liability whatsoever for any loss arising from any use of this material or its contents. This material may not be reproduced, distributed or published without prior written permission from Legg Mason. Distribution of this material may be restricted in certain jurisdictions. Any persons coming into possession of this material should seek advice for details of, and observe such restrictions (if any).

This material may have been prepared by an advisor or entity affiliated with an entity mentioned below through common control and ownership by Legg Mason, Inc. Unless otherwise noted the “$” (dollar sign) represents U.S. Dollars.

This material is only for distribution in those countries and to those recipients listed.

In the UK this financial promotion is issued by Legg Mason Investments (Europe) Limited, registered office 201 Bishopsgate, London, EC2M 3AB. Registered in England and Wales, Company No. 1732037. Authorised and regulated by the UK Financial Conduct Authority.

ClearBridge is a Legg Mason affiliate with a focus on quality focused equity.

Legg Mason is one of the world’s largest global asset managers.

Scott Glasser, Co-Chief Investment Officer, Managing Director, Portfolio Manager, ClearBridge

Scott has 28 years of investment industry experience and is a member of ClearBridge's Management, Valuation and Risk Management Committees.

Prior to joining the firm, Scott was a credit analyst specializing in fixed income investments for Bear Stearns. In 1993, Scott joined the research department of predecessor organization Shearson Lehman Brothers as a consumer analyst and transitioned into a role as a portfolio manager one year later.

Scott has a BA in Political Science and Spanish and an MBA in Finance from Pennsylvania State University.

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on treated as a substitute for specific advice of any kind.

We make no warranties, representatives or undertakings about any of the content of this website (including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representation warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Scott Glasser

Scott has 28 years of investment industry experience and is a member of ClearBridge's Management, Valuation and Risk Management Committees. Prior to joining the firm, Scott was a credit analyst specializing in fixed income investments for Bear Stearns. In 1993, Scott joined the research department of predecessor organization Shearson Lehman Brothers as a consumer analyst and transitioned into a role as a portfolio manager one year later. Scott has a BA in Political Science and Spanish and an MBA in Finance from Pennsylvania State University.

Read more articles by this author

Be the first to hear news and insights from Embark Group

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.