Savings rates have trebled in 12 months, and UK savers can earn over 5% on one-year deposits. So doesn’t it make sense to cut risk and stick to the safety of cash?

Cash savers are benefiting from the highest returns in almost two decades, with some popular accounts like cash ISAs currently paying over 5%. The rise in returns has been rapid, with rates today many times higher than a year ago. Unsurprisingly savers are committing more to cash ISAs than at any point in the past five years*.

After a long spell in which nominal returns on cash were virtually zero, investors are now rethinking the role deposits should play in wider portfolios. Schroders’ May 2023 survey of financial advisers – coming as the Bank of England raised interest rates for the 12th time since the start of 2022 – found nine in ten advisers were “having conversations with clients about long-term investing versus cash deposits”.

Aren’t investors right to reconsider cash?

All savers’ circumstances are different, and some may have excellent reasons to be holding cash. But just because savings rates are rising does not mean cash is keeping pace with inflation.

Popular UK savings rates vs inflation

| Cash ISAs | Jan 2022 | June 2022 | Jan 2023 | 30 April 2023 |

| Variable rate | 0.3% | 0.6% | 1.7% | 2.3% |

| 2-year fixed rate | 0.5% | 1.6% | 3.9% | 4.1% |

| Inflation | 5.5% | 9.4% | 10.1% | 8.7% |

Source: Bank of England; ONS, June 2023

As shown, cash returns after inflation – or “real” returns – remain negative, even though rates have risen strongly. Negative returns mean losses. And the jump in inflation since early 2022 means that the value of cash is now eroding at a faster pace than for most of the previous decade, even if the cash earns today’s top available rates.

So for many the key question of where to make long-term investments remains as relevant as ever. In fact it is even more important.

Cash or equities: what are the chances of beating inflation?

The certainty offered by cash lies only in its nominal value. £100 today will still be £100 in future years. There is no certainty its spending power will hold up, however. Low inflation will see the money retain its spending power to some degree, but high inflation will erode it quickly.

Time is the critical factor. Over short periods cash is likely to fare better against inflation. Over long periods, cash fares worse, even where inflation is relatively low.

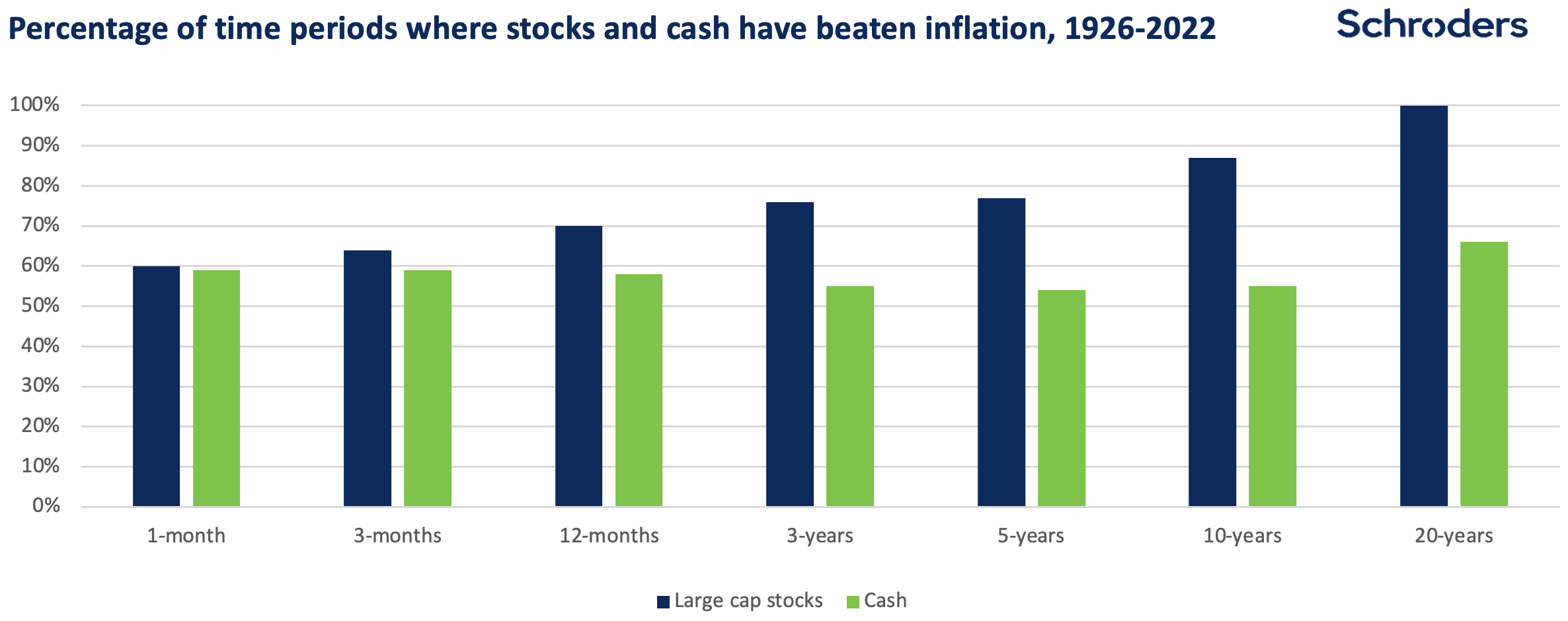

The chart below crunches historic returns on cash and stock market investments over a range of timeframes extracted from 96 years’ data. It then sets these against inflation over the same timeframes.

The results are stark. The chart shows that over very short periods – three months or less – there has not been much difference in the likelihood of cash or shares beating inflation. But for longer periods the gap widens conclusively.

- The likelihood of cash savings beating inflation has been about 60:40 for the majority of all timeframes.

- The likelihood of stock market investments beating inflation has reached 100% where the investments are held for 20 years.

In other words, for every 20-year timeframe in the past 96 years, equities delivered inflation-beating returns.

So while stock market investments may be risky in the short run, when viewed against inflation they have offered far more certainty in the long run.

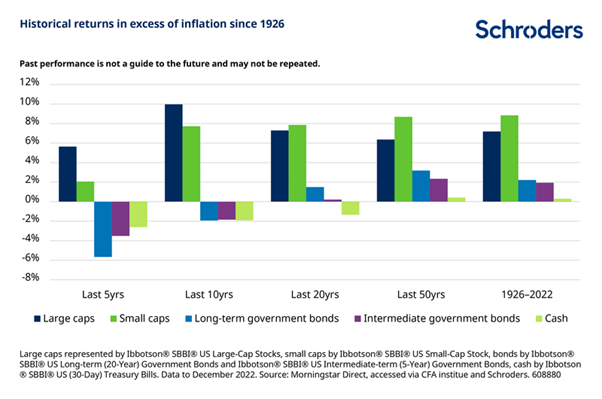

The stock market has delivered strong long-term returns through very different conditions

The recent era of ultra-low interest rates, from which we’re now emerging, has meant that cash has been unattractive for investors. That is despite the fact that inflation until recently has been low.

In the past five, ten and 20 years, cash savings have failed to keep up with price rises and so depositors would be worse off.

Over very long periods – during which inflation and interest rates have gone through both highs and lows – cash has retained its spending power, but only just.

By contrast, stock market investments have delivered inflation-beating returns over all periods highlighted in the chart.

So it’s a no-brainer: stock market investments are a better bet for long-term real returns?

There are lots of reasons to hold cash, and savers’ individual timeframes will differ. For many, this is where financial advice will be invaluable.

“The cash debate is a perfect example of where advisers deliver value to clients,” says Gillian Hepburn, Schroders’ Head of UK Intermediary Solutions. “The question of ‘should I invest in cash?’ is not straightforward, and for the longer-term saver all the data points to investing being the best option for many.

“Investors view ‘trust and peace of mind’ as being a key benefit of receiving advice," she adds. "This is a classic area where clients need ongoing support and where advisers can really deliver that ‘peace of mind’, as well as helping ensure clients’ investments are in the right place to meet their goals.”

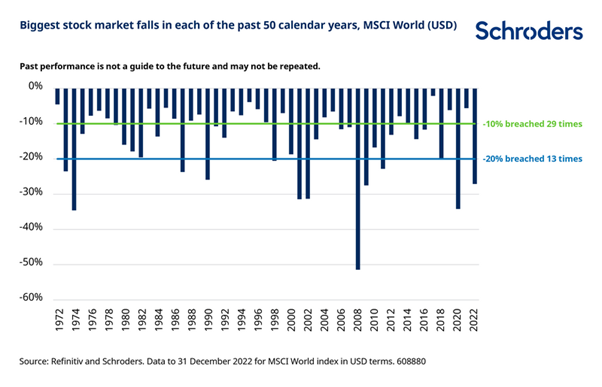

While long-term historic data strongly suggests stock market investments stand a better chance of beating inflation than other investments, they are also volatile.

So investors who opt for stock markets over cash need to be prepared for a bumpy ride.

- In approximately half of the past 50 years markets fell by at least 10%.

- In a quarter of the past 50 years markets fell by at least 20%.

In conclusion, different risks attach to both cash and stocks and shares. Cash is far from a risk-free asset: even at today’s best available savings rates, deposits are likely to lose real value. And, as our data shows, cash can deliver real losses over longer periods too, including the past two decades. But shares also carry risk, especially when held for shorter periods.

*Source: Bank of England, two-year fixed rate cash ISA, change from 30 April 2022 (1.19%) to 30 April 2023 (4.12%). ISA deposits from BoE Money & Credit tables. Data issued June 2023.

Important information

Please remember that the value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested

This marketing material is for professional clients or advisers only. This site is not suitable for retail clients.

Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England.

Schroder Unit Trusts Limited is an authorised corporate director, authorised unit trust manager and an ISA plan manager, and is authorised and regulated by the Financial Conduct Authority.

On 17 September 2018 our remaining dual priced funds converted to single pricing and a list of the funds affected can be found in our Changes to Funds. To view historic dual prices from the launch date to 14 September 2018 click on Historic prices.

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on or treated as a substitute for specific advice of any kind.

We make no warranties, representations or undertakings about any of the content of this website; including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representations, warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Duncan Lamont, Head of Strategic Research, Schroders

Duncan writes actionable, thought leadership research to offer insights which help Schroders’ clients make better investing decisions. Prior to joining Schroders seven years ago, Duncan was a principal in the Global Asset Allocation team at Aon Hewitt, where he was responsible for the development of the firm’s long term strategic capital market assumptions, and driving its medium term asset allocation views across the full range of traditional and alternative asset classes. He also had spells as an assistant director at a corporate finance boutique and as a trainee investment consultant. Duncan is a CFA charterholder with a Masters in Mathematics, Operational Research, Statistics and Economics from the University of Warwick, specialising in actuarial and financial mathematics.

Read more articles by this author

Related Posts

thumbnail image")

AI has a dream (and it’s not about Electric Sheep)

Jun 28, 2023

Generative AI has captured the public imagination since the public release of ChatGPT-3 in November 2022. Users have been able to use generative AI to code, complete homework, and even create award winning photographs, but ChatGPT is not the only contender in the ring. Sajeer Ahmed, Aegon AM, explores the potential for generative AI contenders currently competing in the market.

Read more

China, the US, and the three-body problem: US-China relations and lessons from history

Jun 27, 2023

The United States’s policy toward China is sometimes described as comprising three parts: the co-operative, the competitive and the adversarial. Each is distinct and influences overall policy toward China. What about predicting the movement of these three influential bodies? Is there a pattern, and so a historical precedent? Is that pattern one that repeats, or does it evolve? Or are we observing chaos?

Read more

Cash investing friend or foe?

Oct 28, 2022

Deciding whether to hold cash or invest in the stock market can be a difficult choice that is typically driven by a risk averse attitude and a more limited capacity for loss. However, any decision to invest in cash can come with serious consequences for long-term growth potential.

Read moreBe the first to hear news and insights from Embark Group

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.