Even seasoned investors were spooked by the market turbulence of the last 12 months. Who can blame them, when global stocks had their best and worst sessions in a decade on consecutive days, as they did a little under a year ago?

Explaining investment risks to clients – and showing them how you manage these risks – is a powerful way to demonstrate the value of advice.

Below are four critical areas for advisers to consider, covering the common risks, the significance of financial personality, the benefits of multi-asset investing, and why the case for staying invested in volatile times is as strong as ever. Further information on each of these areas can be found through our new Managing Investment Risk in Volatile Markets hub.

Explaining why you make certain investment recommendations

Periods of market turmoil offer a chance to show clients how investment risk fluctuates, and to showcase the value of advice.

Investment risks range from liquidity and longevity risks to seismic events such as the Covid-19 pandemic. They can overlap and interact. Unhelpfully, the same risks don’t always share the same name, depending on where you look.

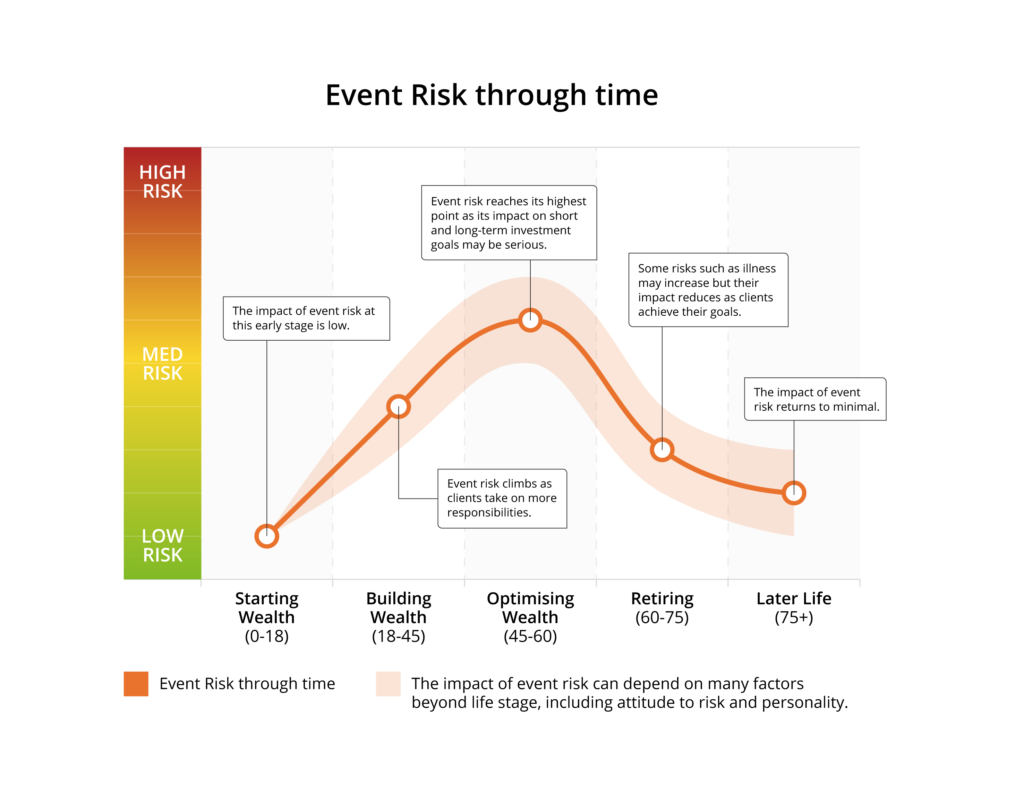

The impact of these investment risks on clients depends on a range of factors, including their immediate and future needs, life stage and personality. It is possible, however, to map the impact each of these risks might have for a typical client as they journey through life and towards retirement. Take event risk, for example:

For each of these it is possible to plot how the risk rises and falls over an investment lifecycle for a typical client.

This can serve as a useful benchmark for why you make the recommendations you do through clients’ life stages. Further detail is available here.

Understanding clients’ financial personality

Clients’ financial ability to take on investment risk depends primarily on their financial circumstances. However, ability doesn’t stop there.

Each investor also has an emotional ability to take risk; a behavioural capacity that determines how best to interact with investments to ensure ongoing comfort with the risk being taken. It doesn’t matter how good a plan is if the person it’s written for doesn’t stick to it or feels sick doing so.

To demonstrate the importance of behavioural capacity, imagine the profiles of three different investors – each with identical risk tolerances and risk capacities.

Where they differ is in three key behavioural traits: composure, confidence, and impulsivity.

Each has a different financial personality and it’s essential to alter your approach to best meet their needs.

For example, clients with traits of low composure and high impulsivity could benefit from auto-investing. Or, for individuals that are confident and highly impulsive, the key is to manage any overconfidence through pre-set review times and frequent, high-level engagement. More information on these profiles and how to manage clients like them is available here.

Showcasing the benefits of multi-asset in unstable markets

Multi-asset funds exist to help manage investment risk. However, while they may sit in a single category, they are not always alike, and some funds can be close to incomparable.

It is worth considering how multi-asset funds underpinned by a stochastic approach to strategic asset allocation can have some unanticipated benefits for investors.

For example, having a long-term outlook can combat market risk by side-stepping the need to adjust weightings prematurely and potentially double down on the negative effects of volatility.

Likewise, stochastic forecasting has become increasingly relevant to retirees, many of whom will almost certainly still be long-term investors.

But, it’s important to recognise that stochastic modelling is a broad brush; not all models capture the range and evolution of investment outcomes.

For example, mean-variance-covariance models are stochastic but describe a distribution around a single ‘deterministic’ path, so are not much good for capturing investment term effects.

Other stochastic models, meanwhile, fail to capture the volatility clustering seen in equities, which has crucial implications for investor risk profiles and sequence risk in drawdown.

Investment decisions should be based on as realistic assumptions as possible, so the model needs to tick a lot of boxes: be forward-looking; capture the term structure of investment returns and the stochastic volatility of equities; and respond proportionately to changing market conditions.

With your clients facing a range of investment risks, the benefits of these stochastic models can be wide-ranging and, in some cases, surprising. More information is available here.

Be prepared to make the case for staying invested

What if an investor had removed risk from their portfolio at the height of the market turbulence last year? What if an investor had stayed the course? What would the outcome have been?

The market turbulence triggered by Covid-19 served to reinforce a famous investment principle followed by Warren Buffett and others.

Take a look at the outcomes for two investors, one advised and one not, between January and October 2020. Each had a long-term investment horizon and a simple portfolio worth £50,000 split equally between equities and fixed interest securities.

While our advised investor, Andy, opted to wait out the market turbulence that began in February 2020, our non-advised investor, Kim, was spooked and acted to de-risk her portfolio. Kim’s portfolio was worth less at the end of the year, despite the decision to de-risk.

As Buffett once said: “We continue to make more money when snoring than when active.”

More information on the power of staying invested is available here.

Conclusion

Understanding that investors are human, and that they need management as individuals, is increasingly crucial during periods of intense instability in the market.

In the words of investor Nicholas Sleep: “For the record, we do not have the faintest idea what share prices will do in the short term – nor do we think it is important for the long-term investor.”

Following the events of this year, and the uncertainty that lies ahead, now may be as good a time as any to remind clients of that.

Read more articles like this via our insights page.

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on treated as a substitute for specific advice of any kind.

We make no warranties, representatives or undertakings about any of the content of this website (including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representation warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Scott Sinclair, Embark Group

Read more articles by this author

Be the first to hear news and insights from Embark Group

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.