There continues to be a remarkable focus on green hydrogen as a clean alternative to traditional fossil fuels, with the past year further accelerating its potential widespread adoption. So, what is driving all this hype, is hydrogen the sustainability disruptor, and why has there been such remarkable recent progress?

What and how?

Hydrogen is the most abundant molecule in the universe, found primarily locked in water and hydrocarbons. Its qualities have been known for a long time, and it has been used for more than 100 years as an industrial chemical. While the concept of hydrogen as a source of energy isn’t novel, it has never been feasible on a large scale – until now.

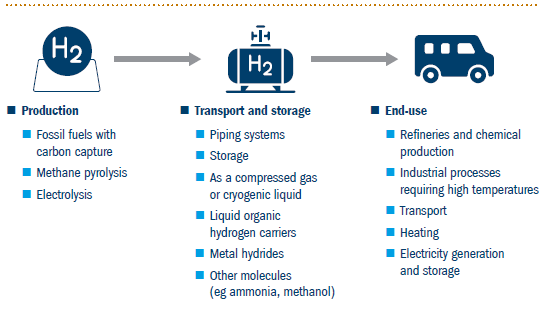

Hydrogen is a colourless gas, but it is categorised by colour, each representing a different production pathway. Grey hydrogen is generated via the use of fossil fuels, so its production emits CO2. Blue hydrogen is grey hydrogen paired with carbon capture and storage that covers the majority of carbon emissions produced in its generation. Green hydrogen, meanwhile, is produced by the electrolysis of water, splitting it into hydrogen and oxygen, and as long as renewable energy is used it is a zero-emission energy source. Thus, if created at scale green hydrogen has the potential to become key in decarbonising hard-to-abate sectors of the economy.

Catalysts for uptake

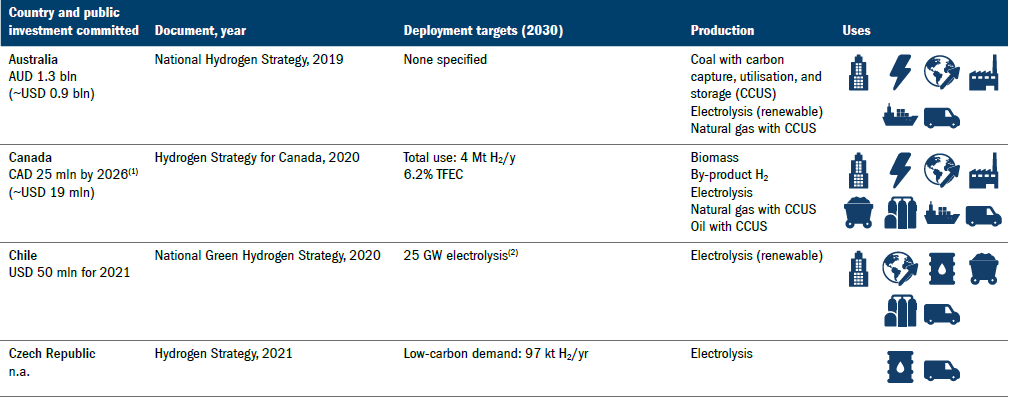

For hydrogen to become a viable solution, both greater demand and reduced costs are required. But we are now seeing movement on three key drivers. Firstly, climate change is accelerating. This feeds directly into a second key driver – policy support for the need to do something about it (Figure 1). Since the Paris Agreement in 2015 governments have turned their attentions to climate change and committed themselves to achieving emissions reduction targets that could lead to carbon neutrality by 2050. The Covid-19 pandemic has only accelerated the urgency surrounding these policies. As policymakers look for ways of cutting emissions, hydrogen technology could be a feasible alternative. Excitingly, the Hydrogen Council suggests hydrogen could reduce global emissions by 6 gigatons – or 17% of global 2020 emissions – by 2050.1 Currently, around 66 countries have net-zero emissions targets, of which around 20 have unveiled hydrogen roadmaps. We expect more to follow.

The third key driver is that green hydrogen prices have fallen dramatically in the past 10 years due to efficiency improvements. The renewable energy used in electrolysis accounts for about 70% of the cost of producing hydrogen and has fallen in price by approximately 70% in the past decade.2 Additionally, the price of an electrolyser has declined by about 60% in that time.3 It is reasonable to expect these price falls will continue, adding to the appeal of green hydrogen.

Figure 1: Governments with national hydrogen strategies; announced targets; priorities for hydrogen and use; and committed funding

Source: IEA (October 2021)

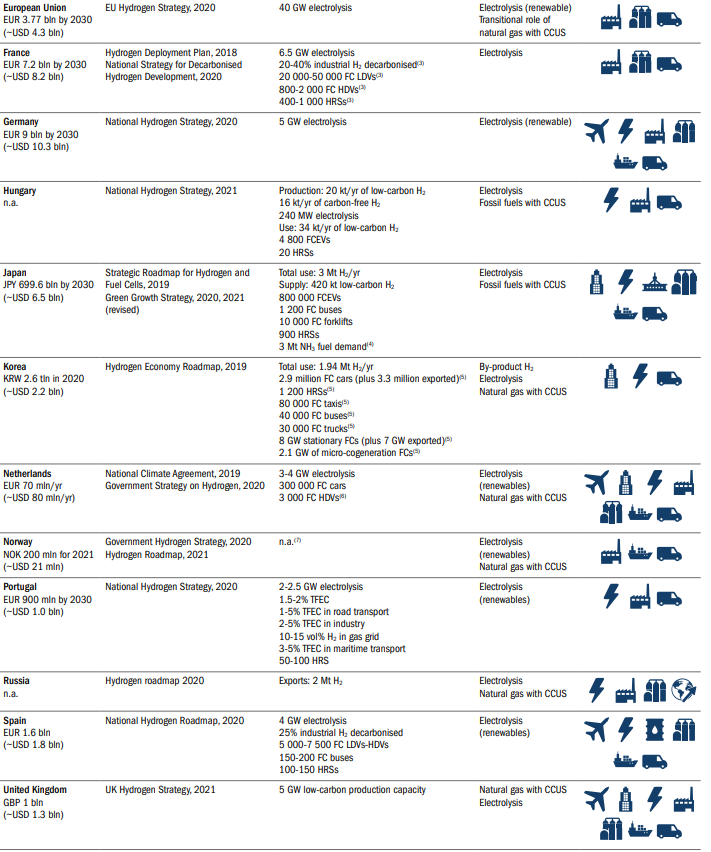

Figure 2: Company and analyst transcript mentions

Source: MS Sept 2021

What has changed in the past 12 months?

While discussion around green hydrogen has seen steady growth, there have been disproportionate levels of debate over the past six and 12 months (Figure 2), far exceeding any other topic including 5G, Blockchain and AI.4 So why the surge of interest?

First and foremost, there is continuing momentum in a number of factors that have been key catalysts for increased uptake over the past decade. Regarding efficiency and costs, 2021 projections suggest reductions in the hydrogen cost curve, while manufacturing scale should support a rapid pick up in adoption from 2030 onwards in many different industries ranging from chemicals to trucking fuel cells.5 A recently revised forecast by Bloomberg puts green hydrogen costs 13% lower than previously suggested by 2030.6 With prices of carbon at high rates globally, and at recent all-time highs within the EU,7 hydrogen’s potential as a significant decarbonisation solution has never had as much commercial viability.

The emergence of multiple exciting hydrogen projects over the past 12 months have been influential in these reduced estimates of cost and efficiency improvements. Between December 2020 and August 2021 alone, the number of green hydrogen projects increased more than three-fold,8 with 359 large-scale projects announced globally. Europe is leading the way with investments of $130 billion, but other regions are catching up. China is also emerging as a potential hydrogen giant with more than 50 projects in the pipeline following its announcement of net-zero emissions by 2060.9

A major cost development came to light in the Q3 2021 report of NEL, the world’s largest electrolyser producer. It had been widely expected that the cost of green hydrogen would be less than $2/kg by 2030.10 But costs are falling rapidly and NEL now has a green hydrogen cost target of $1.50/kg by 2025. This illustrates the pace of innovation within green hydrogen and continued decline in the cost of renewables globally.

Arguably the most influential element in the progress of green hydrogen production as a sustainability disruptor is government support. Simply put, governments across the world need a plan for life after fossil fuels, and their ability to create policies and regulations to support green hydrogen both financially and in terms of infrastructure could prove vital in its viability. It is one thing producing green hydrogen at a cost of $1.50/kg, but for uptake to be aligned with net-zero targets it needs to be delivered to the end customer at a price that is competitive with fossil fuels. Infrastructure is needed to facilitate this process.

In the past year, the Chinese government has made $20 billion of public funding available for hydrogen projects. So far, 50% of its announced projects are linked to transport applications, a key sector in its energy transition plan.11 Meanwhile, the US has renewed its net-zero commitment by re-entering the Paris Agreement following President Biden’s inauguration.12

In August 2021, the UK government set its sights on developing a thriving green carbon sector to overcome the decarbonisation challenges facing its economy, in the form of the UK Hydrogen Strategy. Its ambition is to build 5GW of low carbon hydrogen production capacity by 2030. This could produce hydrogen equivalent to the amount of gas consumed by more than three million households in the UK each year.13 The UK Hydrogen Strategy is all encompassing and takes a holistic approach to developing a thriving hydrogen sector. It sets out what needs to happen to enable the production, distribution, storage and use of hydrogen, and to secure economic opportunities across the UK.14

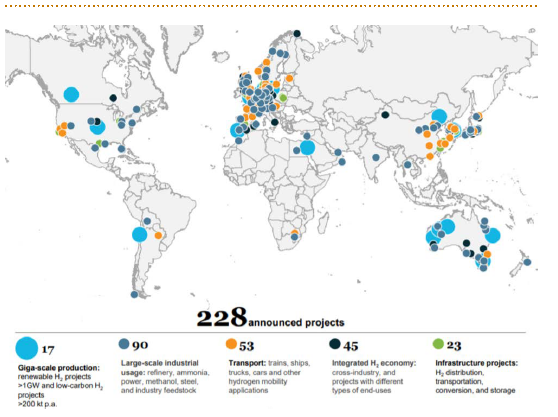

Figure 3: Private equity, infrastructure and hydrogen

Source: Morgan Stanley – The Hydrogen Handbook. The Hydrogen Council.

Figure 4: Identifying infrastructure investments across the hydrogen value chain

Source: Arup Hydrogen

We are beginning to see an emergence of companies specialising in the production, distribution and usage of Hydrogen. Globally there are 228 ongoing hydrogen projects across the value chain (Figure 3), 17 of which are giga-scale production schemes. Two notable recent acquisitions are of the Canadian electrolyser company Hydrogenics for $290 million15 by power firm Cummins, and MAN Energy Solutions’ majority share in Germanbased electrolyser manufacturer H-TEC Systems for an undisclosed fee.16

Interestingly, we are also seeing investment in riskier early-stage hydrogen start-ups focused on the non-electrolysis production of hydrogen. The funding of such project development and integration services could be indicative of a maturing sector.17 The Hydrogen Council estimates total investment in the hydrogen value chain could exceed $300 billion by 2030 and, according to the Energy Transitions Commission, reach approximately $15 trillion by 2050.18 This demonstrates both the requirement of, and opportunity for, private investment within the chain (Figure 4).

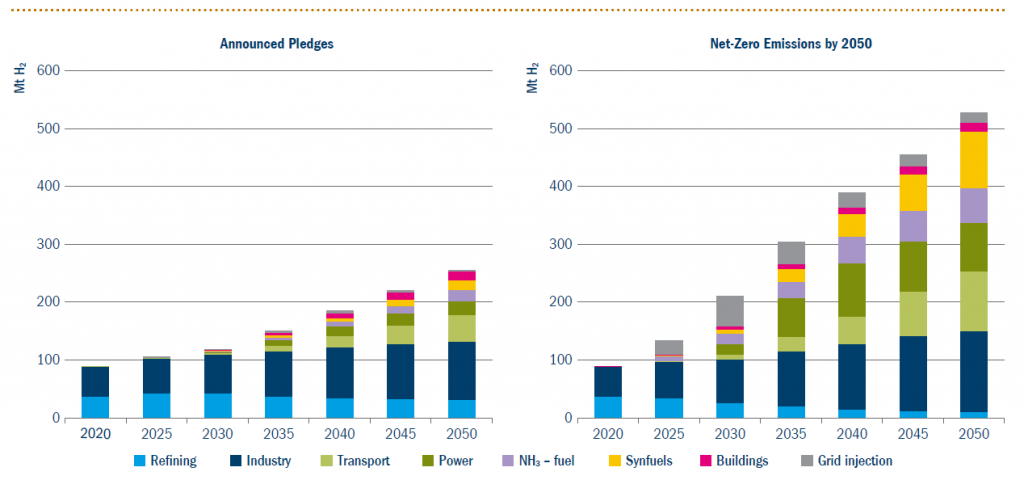

While there are multiple barriers for the uptake of hydrogen within the mainstream – from cost to efficiency – we believe there are two main ones. The first is current limited demand. While from a production perspective policy support is expanding, technology is improving and cost is going down, there is still a limited actual demand for the molecule. Net-zero pledges could however bolster demand (Figure 5). Further infrastructure development will be a critical determinant as to whether green hydrogen becomes the panacea of decarbonisation.

Second is the underappreciation of hydrogen within society. There has been a stigma surrounding its use as a fuel ever since the Hindenberg disaster in 1937. Consumers and investors must be made aware of the promise and safety of hydrogen before it enters the mainstream. We believe asset managers are becoming increasingly aware of its potential and are attempting to educate their investors. We hope the public can be educated in much the same way. We believe there is a huge opportunity for the infrastructure sector in all of this: without infrastructure projects, there will be no mainstream consumption of hydrogen.

Figure 5: Hydrogen demand in the IEA’s Announced Pledges and Net-Zero Emissions scenarios

Source: IEA: 2021 Hydrogen Review

Conclusion

The opportunity for green hydrogen to disrupt the sustainable energy industry cannot be denied – from increasing technological improvements to scalability and policy support, the past 12 months have witnessed huge advancements – and the pace at which it could do so must not be underestimated. On a walk down New York’s Fifth Avenue in 1900 you would likely have seen 1,000 horses and one automobile. Just a decade or so later it’s likely the opposite was the case. In 1900 the car was inefficient, unreliable and expensive versus the horse, but the long-term opportunity was salient. Perhaps a decade from now we will be questioning why there was ever a debate about hydrogen.

Lack of demand is currently the main barrier for the mainstream consumption of hydrogen. While policy support is growing exponentially, it is not close to the level needed to achieve net-zero energy system emissions by 2050.

A mixture of such support, through incentivisation mechanisms for the utilisation of hydrogen and development of infrastructure, will be vital. Signs of growing investment in the latter are positive. However, to retain this momentum policy will need to focus not just on reducing costs but on creating supporting infrastructure to ensure demand. Policy support is strong, as illustrated in Figure 1, but there is scope for more, especially as countries outline their net-zero goals. The recent rise in energy prices may fast-track policies in the next 12 months. Post-COP26 we should have better insights around policy support, and we may be able to identify prominent, fruitful infrastructure opportunities.

Notes

1Morgan Stanley Research: The Hydrogen Handbook.

2Kepler Cheuvreux, All About Hydrogen, September 2020/Goldman Sachs, Carbonomics, The rise of clean hydrogen, July 2020.

3BNEF, Hydrogen Economy Outlook, March 2020.

4Morgan Stanley Research: The Hydrogen Handbook.

5Morgan Stanley Research: The Hydrogen Handbook.

6Fuel Cell Works – https://fuelcellsworks.com/news/green-hydrogen-is-on-track-to-be-cheaper-than-natural-gas-by-2050-bnef/

7SP Global – https://spglobal.com/platts/en/market-insights/latest-news/energy-transition/082721-eu-carbon-prices-power-up-to-new-all-time-high

8Statista – https://statista.com/statistics/1011849/largest-planned-green-hydrogen-projects-worldwide/

9Hydrogen Insight Updates July 2021 – https://hydrogencouncil.com/en/hydrogen-insights-updates-july2021/

10Green hydrogen will be cost-competitive with grey H2 by 2030 — without a carbon price’ – Recharge News.

11Hydrogen Council – Updates July.

12https://state.gov/the-united-states-officially-rejoins-the-paris-agreement/

13UK Hydrogen Strategy https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1011283/UK-Hydrogen-Strategy_web.pdf

14UK Hydrogen Strategy – https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1011283/UK-Hydrogen-Strategy_web.pdf

15Cummins closes on its acquisition of Hydrogenics https://cummins.com/news/releases/2019/09/09/cummins-closes-its-acquisition-hydrogenics

16MAN Energy Solutions is replacing GP JOULE as the main owner of H-TEC SYSTEMS – https://man-es.com/company/press-releases/press-details/2021/06/16/man-energy-solutions-is-replacinggp-

joule-as-the-main-owner-of-h-tec-systems

17Global Hydrogen Review 2021.

18Catalysing hydrogen investment – ARUP.

About the authors

Benjamin Kelly, Senior Thematic Analyst, Columbia Threadneedle Investments

Benjamin Kelly is a Senior Thematic Analyst (Behavioural Economics), Responsible Investment at Columbia Threadneedle Investments. His principal responsibility relates to the development, delivery and integration of thematic research within the context of responsible investment strategies, in particular sustainable outcome strategies across equity and fixed income portfolios. Within these strategies he is also involved in the wider work of the team around environmental, social & governance (ESG) research, voting, reporting and engagement. In addition, Ben leads the team’s idea generation in behavioural science from a thematic and governance perspective which includes providing behavioural insights to the investment teams regarding biases in investment decision making.

Prior to joining the company, Ben worked in BlackRock’s Investment Institute where he combined macroeconomic research across equity, fixed income and real asset teams with expertise in behavioural finance and investment decision making. In this context, he worked with fundamental and quantitative alpha generation teams focusing on their investment processes and how these can be modified to combat behavioural biases. Ben is a current visiting lecturer in behavioural science at the University of St. Andrews and London School of Economics.

Heiko Schupp, Global Head of Infrastructure Investments, Columbia Threadneedle Investments

Heiko is Global Head of Infrastructure Investments, bringing over 23 years of relevant industry experience. He leads all unlisted Infrastructure investment and fundraising activities and heads up the investment team. He also leads internal and external stakeholder engagements. Prior to joining Columbia Threadneedle, Heiko was the Portfolio Manager of Hastings Fund Management’s Core Infrastructure Income Fund, the first European domiciled open-ended infrastructure Fund and a member of Hastings’ Management Board and Investment Committee.

He co-led Pantheon’s US$500 million infrastructure investment programme, which focused on co-investment, secondary and primary fund-of-funds investment activities. Heiko holds a Masters in Economics from Polytechnic University of

Koblenz.

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on or treated as a substitute for specific advice of any kind.

We make no warranties, representations or undertakings about any of the content of this website; including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representations, warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Columbia Threadneedle Investments

Columbia Threadneedle Investments is a leading global asset management group that provides a broad range of actively managed investment strategies and solutions for individual, institutional and corporate clients around the world.

Read more articles by this author

Be the first to hear news and insights from Embark Group

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.