With markets experiencing their worst falls since the global financial crisis, we believe focusing on long-term themes is more important than ever for investors. Here we outline a pragmatic view of the current situation and how our investment philosophy enables a balanced and opportunistic response to market conditions.

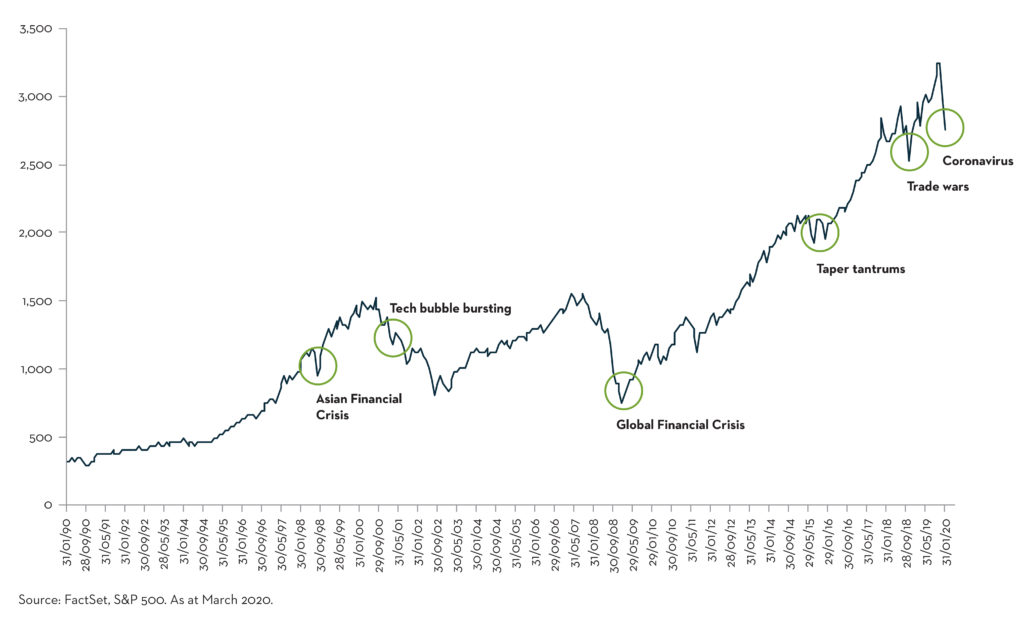

Historic market context

The ‘black swan’ event of the coronavirus is bringing high risk of downside to the economic momentum globally, and therefore to corporate earnings in the short term. The magnitude of the downside risk is difficult to quantify at this stage, being dependent on how long and how severely the virus crisis is going to impact economic activity.

As a result of this fear and increased uncertainty, equity markets have significantly repriced globally from historically high valuations. However, it is worth considering this event in an historic context against other prominent market falls and the overall upward trajectory of share prices in the last thirty years.

Source: FactSet, S&P 500. As at March 2020. Past performance is no guarantee of future results. Indexes are unmanaged, and not available for direct investment. Index returns do not include fees or sales charges. This information is provided for illustrative purposes only and does not reflect the performance of an actual investment.

Immediate economic outlook

The impact of the virus is undoubtedly globally significant in the short term, constituting both a supply and demand shock at the same time.

Beyond China’s growth figures, which will be particularly badly hit, supply chains and global GDP will also be severely impacted, with Europe likely to suffer more than the US. At the market level, investors could remain in fear mode for a while.

However, this downward pressure in economic momentum is likely to trigger sizeable and potentially globally synchronized policy responses in the next 6-9 months to ensure the world doesn’t dip into a recession.

Central banks are on stand-by to act in an even more accommodative manner (and have in some instances already started to act), should economic activity suffer too much from the pandemic fear. We are also likely to see sizeable fiscal policy responses across key economies. Both of these could trigger a positive market response.

Market reaction

Markets are likely to remain in fear mode for several weeks. We predict 2020 will continue to be volatile given both the short-term headwinds to growth and earnings, and the likely supportive monetary and fiscal measures we might see.

There will therefore certainly be plenty for the short-term pessimists to focus on. Depending on risk appetite, the market may or may not be willing to look through the sizeable earnings downgrade risk and profit warnings coming up in Q1 and potentially Q2, possibly leading to the need to reduce 2020 estimates. In the coming months, it will be a period of hoping for economic activity to recover in the second half of the year.

We believe markets will bottom once evidence of policy response comes through, once pandemic threat eases (contagion risk plateauing, hopes of a vaccine fast-tracked to availability) and/or the short-term negative impact on economic and corporate activity is accounted for.

Conclusion

Short-term investors will focus on the earnings downgrades to come at quarterly results, but for long-term investors, we see this period as an opportunity to buy selected stocks at more favourable entry points than previously.

A clear focus on quality businesses with strong balance sheets, pricing power, high returns and sustainable business models helps withstand short-term downward pressure, while accessing the economic benefits of longer-term growth themes.

We have identified three megatrends which we believe are going to be driving market dynamics across a range of industries, long after the current share price slump has passed: Demographic Change; the Future of Technology; and Resource Scarcity.

These are mega-trends that will remain relevant on a multidecade perspective and we will therefore look to use this valuable time to seek out companies that are long-term beneficiaries of these themes at attractive valuations.

Read more from our Insights page

Definitions

The Asian financial crisis was a period of financial crisis that gripped much of East Asia beginning in July 1997 and raised fears of a worldwide economic meltdown due to financial contagion.

The black swan theory or theory of black swan events is a metaphor that describes an event that comes as a surprise, has a major effect, and is often inappropriately rationalized after the fact with the benefit of hindsight

A central bank is a national bank that provides financial and banking services for its country's government and commercial banking system, as well as implementing the government's monetary policy and issuing currency.

The Global Financial Crisis (GFC) – also known as the financial crisis of 2007–08, the global financial crisis and the 2008 financial crisis – was a severe worldwide economic crisis considered by many economists to have been the most serious financial crisis since the Great Depression of the 1930s, to which it is often compared.

FactSet Research Systems provides computer-based financial data and analysis for financial professionals, including investment managers, hedge funds, and investment bankers.

Gross Domestic Product (GDP) is an economic statistic which measures the market value of all final goods and services produced within a country in a given period of time.

A pandemic is the worldwide spread of a new disease.

The S&P 500 Index is an unmanaged index of 500 stocks that is generally representative of the performance of larger companies in the U.S.

“Taper tantrum” refers to the financial markets’ reactions, in May-August 2013, to the announcement by the Federal Reserve that it was planning to decrease, or “taper” its $70 bn per month bond buying program.

The tech bubble (also known as the dot-com bubble and the Internet bubble) was a stock market bubble caused by excessive speculation in Internet-related companies in the late 1990s.

Trade wars refers to the China–United States trade war, which began in 2018 and is an ongoing economic conflict between the world's two largest national economies, China and the United States.

Forecasts are inherently limited and should not be relied upon as indicators of actual or future performance.

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on treated as a substitute for specific advice of any kind.

We make no warranties, representatives or undertakings about any of the content of this website (including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representation warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Zehrid Osmani

Zehrid is Head of the Global Long-Term Unconstrained team and is also co-manager of Martin Currie Global Portfolio Trust. He joined Martin Currie in May 2018 from BlackRock, where he held a number of senior roles from January 2008. At BlackRock, he was a senior portfolio manager and had responsibility for managing several pan-European equity funds with a specific focus on unconstrained, high-conviction, long-term portfolios, as well as being Head of European Equities Research. Prior to this, Zehrid managed equity portfolios at Scottish Widows Investment Partnership (SWIP), and was a specialist sector analyst at Commerzbank Securities, UBS Warburg and Credit Lyonnais. Zehrid began his investment career as a trainee fund manager at Scottish Investment Trust. He has a BA in Economics and Finance from University of Paris-Sorbonne and a Masters in International Finance from the University of Glasgow.

Read more articles by this author

Be the first to hear news and insights from Embark Group

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.