Key takeaways

- While the manufacturing contraction could marginally worsen due to trade tensions and slower capex, the consumer side of the economy should remain strong enough to avert recession.

- The likelihood of continued volatility in 2020 steers us to high-quality growth companies with strong moats around their businesses and to more defensive sectors that have tended to hold up well during turbulent periods.

- Several indicators related to the presidential election cycle and periods following a yield curve inversion suggest the bull market will continue into next year.

Consumer strength should avert recession as equity markets remain volatile

The S&P 500 Index made new all-time highs in 2019, as on-and-off trade tensions with China eased, the Federal Reserve (Fed) cut interest rates three times and corporate earnings held up better than anticipated. Strong market performance came against a backdrop of weakening economic activity, reflected in the overall signal for the ClearBridge Recession Risk Dashboard turning yellow in June, indicating caution. As we enter 2020, both the U.S. and global economies are clearly slowing; the key question is whether we are on the cusp of a recession or a late-cycle slowdown. The economy typically sees an inflection point six to nine months after the dashboard turns yellow, so we should have confirmation by early next year of the severity of the current soft patch.

Our base case is for a slowdown within an ongoing economic expansion. While we expect the contraction of the manufacturing sector to marginally worsen as the ongoing trade war hurts business confidence and slows capex, the consumer side of the economy should remain strong enough to avert recession. The labour market and wage growth are healthy - although wage pressure is mounting among lower paid employees - which should underpin consumer spending, while the Fed has joined with central banks around the world in ramping up monetary accommodation.

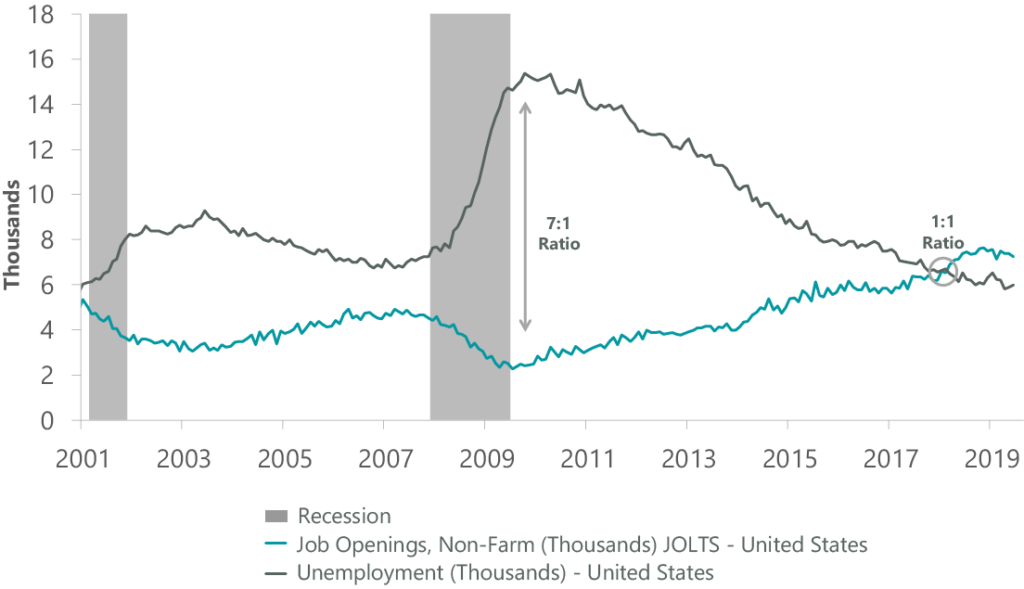

This consumer strength is reflected by all four consumer indicators in the dashboard flashing green, indicating expansion. After slowing in line with rising mortgage rates, housing permit growth has resumed since the Fed shifted its monetary policy stance and mortgage rates eased. Strong job numbers in October and November are consistent with jobless claims continuing to trend around 50-year lows while job sentiment has improved after a mid-year decline, with job openings outnumbering unemployed workers by a significant margin (Exhibit 1). The wildcard among our consumer indicators is retail sales, which posted a surprise decline in September before rebounding in October. Monthly sales numbers can be noisy, but a drop in spending – which accounts for 70% of the U.S. economy – would be a major concern.

Exhibit 1: Job openings vs. Unemployed

Sources: FactSet, U.S. Department of Labor and National Bureau of Economic Research. Data as of 8/31/2019, latest available as of Sept. 30, 2019. Past performance is no guarantee of future results. Indexes are unmanaged, and not available for direct investment. Index returns do not include fees or sales charges. This information is provided for illustrative purposes only and does not reflect the performance of an actual investment.

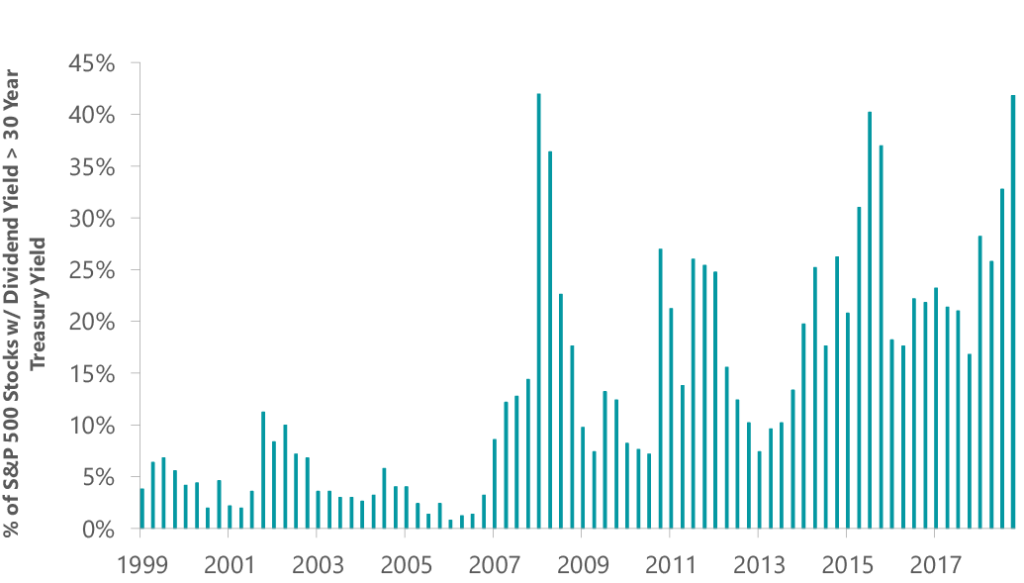

Cyclicals have gotten a bid from the Fed easing, but this rally could be short-lived as we do not believe the manufacturing side of the economy is out of the woods yet. For example, corporate credit spreads at the lowest quality ratings, which encompass energy, industrials and some retail names, are at their widest levels in over a year. Instead, the likelihood of continued volatility in 2020 steers us to high-quality growth companies with strong moats around their businesses and more defensive areas of the market that have tended to hold up well during turbulent periods. Consumer staples and utilities should continue to lead unless we see a clear resolution of the trade war and improving global growth. One of the benefits of these stocks is dividends. Through the third quarter of 2019, 42% of S&P 500 stocks had a higher dividend yield than the 30-year U.S. Treasury bond.

Exhibit 2: Dividend paying equities look attractive

Source: FactSet, as of 9/30/2019. Past performance is no guarantee of future results. Indexes are unmanaged, and not available for direct investment. Index returns do not include fees or sales charges. This information is provided for illustrative purposes only and does not reflect the performance of an actual investment.

While volatility will likely remain elevated, a market drawdown next year is not imminent. In fact, over the last 19 U.S. presidential election cycles, stocks have suffered losses just twice in the 12 months leading up to election day, delivering an average return of 8%. Equities have also tended to do well in periods following a yield curve inversion, especially if no recession occurs, rising 13.5% on average in the subsequent 12 months. The 2-year/10-year U.S. Treasury yield curve inverted in August, suggesting that stocks could climb through most of next year.

About Legg Mason

Legg Mason is one of the world’s largest global asset managers, bringing you expertise across equities, fixed income and alternatives. We have nine independent, specialist investment managers, each with their own objective thinking. This means we offer you a choice of strategies and vehicles to help you to diversify your clients’ investments and deliver outcomes that meet their goals.

ClearBridge is a Legg Mason affiliate with a focus on quality focused equity. Read more about ClearBridge.

Important Information

All investments involve risk, including possible loss of principal.

The value of investments and the income from them can go down as well as up and investors may not get back the amounts originally invested, and can be affected by changes in interest rates, in exchange rates, general market conditions, political, social and economic developments and other variable factors. Investment involves risks including but not limited to, possible delays in payments and loss of income or capital. Neither Legg Mason nor any of its affiliates guarantees any rate of return or the return of capital invested.

Equity securities are subject to price fluctuation and possible loss of principal. Fixed-income securities involve interest rate, credit, inflation and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed income securities falls.

International investments are subject to special risks including currency fluctuations, social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Commodities and currencies contain heightened risk that include market, political, regulatory, and natural conditions and may not be suitable for all investors.

Past performance is no guarantee of future results. Please note that an investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

The opinions and views expressed herein are not intended to be relied upon as a prediction or forecast of actual future events or performance, guarantee of future results, recommendations or advice. Statements made in this material are not intended as buy or sell recommendations of any securities. Forward-looking statements are subject to uncertainties that could cause actual developments and results to differ materially from the expectations expressed. This information has been prepared from sources believed reliable but the accuracy and completeness of the information cannot be guaranteed. Information and opinions expressed by either Legg Mason or its affiliates are current as at the date indicated, are subject to change without notice, and do not take into account the particular investment objectives, financial situation or needs of individual investors.

The information in this material is confidential and proprietary and may not be used other than by the intended user. Neither Legg Mason or its affiliates or any of their officer or employee of Legg Mason accepts any liability whatsoever for any loss arising from any use of this material or its contents. This material may not be reproduced, distributed or published without prior written permission from Legg Mason. Distribution of this material may be restricted in certain jurisdictions. Any persons coming into possession of this material should seek advice for details of, and observe such restrictions (if any).

This material may have been prepared by an advisor or entity affiliated with an entity mentioned below through common control and ownership by Legg Mason, Inc. Unless otherwise noted the “$” (dollar sign) represents U.S. Dollars.

This material is only for distribution in those countries and to those recipients listed.

In the UK this financial promotion is issued by Legg Mason Investments (Europe) Limited, registered office 201 Bishopsgate, London, EC2M 3AB. Registered in England and Wales, Company No. 1732037. Authorised and regulated by the UK Financial Conduct Authority.

Jeff Schulze, CFA, Investment Strategist

Jeff is an Investment Strategist and oversees capital market and economic research, contributing thought leadership on these topics that is frequently quoted in the financial media, including the Wall Street Journal, CNBC and CNN. He joined ClearBridge Investments in 2014 and has 14 years of investment industry experience. Prior to joining ClearBridge, Jeffrey was a Portfolio Specialist at Lord Abbett & Co., LLC. He received a BS in Finance from Rutgers University. He is a member of the CFA Institute.

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on treated as a substitute for specific advice of any kind.

We make no warranties, representatives or undertakings about any of the content of this website (including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representation warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Jeff Schulze

Jeff is an Investment Strategist and oversees capital market and economic research, contributing thought leadership on these topics that is frequently quoted in the financial media, including the Wall Street Journal, CNBC and CNN. He joined ClearBridge Investments in 2014 and has 14 years of investment industry experience. Prior to joining ClearBridge, Jeffrey was a Portfolio Specialist at Lord Abbett & Co., LLC. He received a BS in Finance from Rutgers University. He is a member of the CFA Institute.

Read more articles by this author

Be the first to hear news and insights from Embark Group

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.