Embark Investor Confidence Barometer

The Troubling Rise of a New Advice Gap

Almost half of advisers intend to give less or cease DB transfer advice

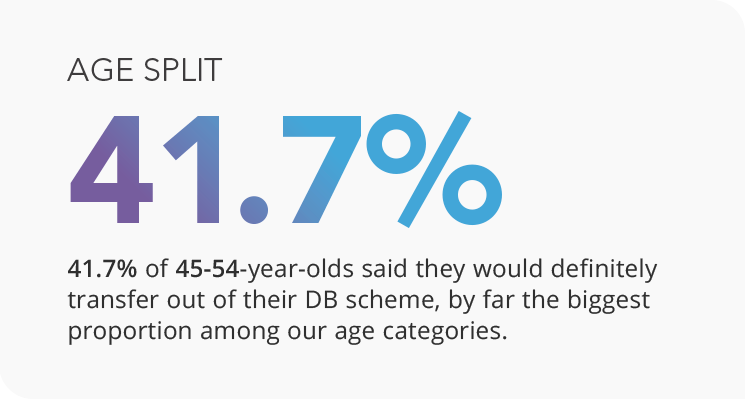

Third of advised consumers with DB benefits would ‘definitely’ transfer

‘Frequently ignored’ behavioural considerations when moving clients out of DB

A ban on contingent charging for defined benefit (DB) pension transfers took effect from 1 October 2020.

Without taking financial advice, an individual with a transfer value over £30,000 cannot transfer their DB pension. If they do take advice, they will pay the same advice fee whether the recommendation is to stay in their scheme or transfer to another arrangement.

Though the move was designed to protect people from being advised to transfer when it isn’t the right path for them, it may also put some people off a DB transfer when, given their circumstances, it may be the best thing for them.

We asked advisers and clients about their plans when it came to DB transfers.

More than seven in 10 advisers (72%) said they are either very confident or somewhat confident in their ability to comply and meet the ban on contingent charging for DB transfers, with almost three in 10 stating they are very confident.

Would you transfer out of your DB scheme?

Percentages taken from 161 advised consumers with a DB pension.![]()

Percentages may not add up to 100 due to rounding

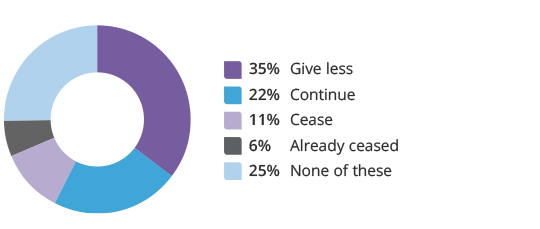

How will the charging ban affect your DB advice offering?

Percentages taken from 250 advisers.

However, almost half (46%) said the ban on contingent charging for defined benefit transfers means they intend to give less DB transfer advice, or cease offering it altogether.

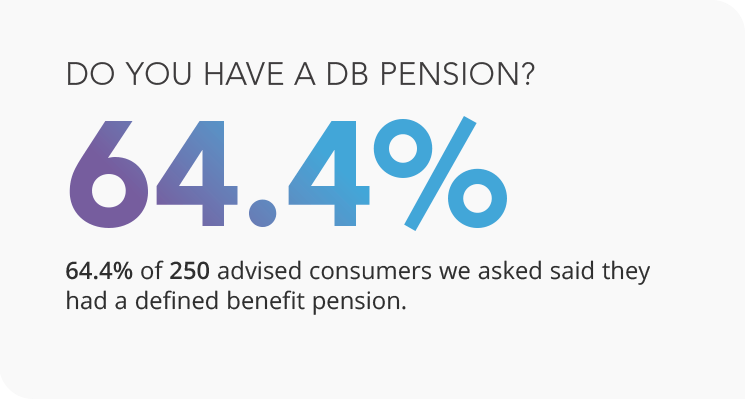

Meanwhile, almost two-thirds of clients have a DB pension and, of those, 30% suggested they wish to transfer the benefits out of their scheme while over half (52%) said they possibly will.

The findings may suggest there is a new advice gap emerging centred as much on advisers’ willingness to offer advice as it is on consumers’ preparedness to pay.

An Expert’s View

“There are huge, and frequently ignored, behavioural considerations when moving out of DB.

For example, the “actuarial” solutions glibly assume the investor will remain invested after transfer and will stick to their spending plans. Both are unlikely to be true, particularly for some personality types.

The financial personality of the investor is at least as important in determining the right advice as the numbers.

For example, clients who score low on composure are far more likely to leave cash uninvested after the transfer. And highly impulsive investors are much less likely to stick to their spending plans. In my view, both make transferring vastly less sensible for these clients, regardless of the financial calculations.

To provide adequate advice on pensions transfers, advisers need to be considering these factors and using robust financial personality measures to accurately diagnose the human components of these important decisions.”

Greg B Davies, PhD

Head of Behavioural Science, Oxford Risk

Contact us

If you have any questions or wish to find out more about the Embark Investor Confidence Barometer, please contact us here.

Download the full guide

Looking to download the full Embark Investor Confidence Barometer? Simply fill out a form and download the guide.