Nine months ago, I wrote a piece arguing why I believe 2020s will be the decade of the cheap asset.

This was at a time financial media was awash with headlines that read ‘the death of value’. We saw this as the market capitulating at the end of a decade long underperformance for the style. After seeing initial recovery last September, and more violent moves since the positive news on COVID vaccines last November, now it would be hard to find a strategy note that doesn’t talk about the great value rotation.

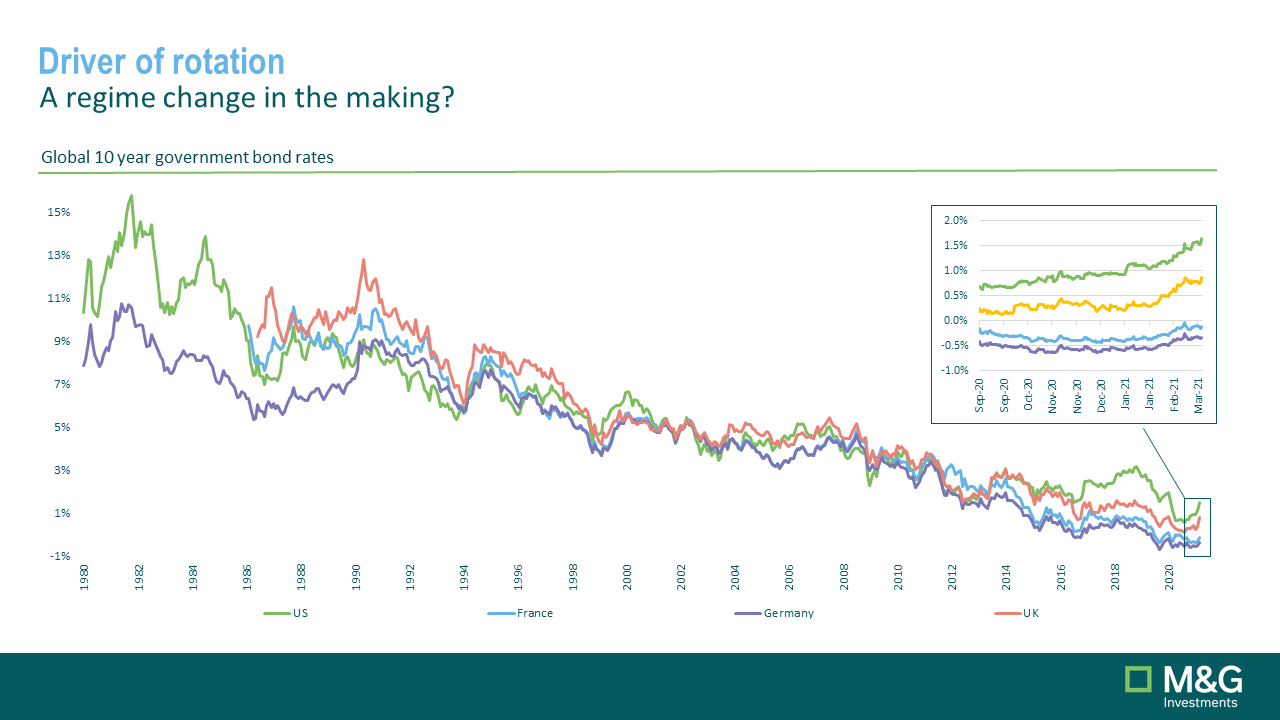

A regime change in the making?

One of the strongest factors that contributed to value’s prolonged underperformance was the 40-year downward trend in global interest rate. It is, thus, not surprising that the rotation back into value is happening as we begin to see rates tick up. Although the recent spike appears quite dramatic, government bond yields are still incredibly low by historical standards. Importantly, in our view, there is little scope for them to go much lower. Therefore, irrespective of whether they rise further, we think the current situation is positive for value. We are optimistic that the prolonged headwind that value has faced over the past ten years from falling bond yields could finally be receding.

[caption id="attachment_26906" align="aligncenter" width="1280"] Global 10 year government bond rates - yellow line in top right represents UK.[/caption]

Global 10 year government bond rates - yellow line in top right represents UK.[/caption]

Another challenge for value has been the rise of monopolistic global companies that continued their exponential growth in recent years. We are seeing evidence of these companies beginning to compete with one another – such as the increasingly overlapping digital content offerings, a potential race for next generation of cars, and even the foray into digital currency. In addition, regulations are catching up with these ‘once-disruptor’ businesses. For example, governments have been investigating debit-card practices and examining the behaviours of social media enterprises.

In our view, these combined trends represent significant opportunities for negative surprises on these over-bid companies.

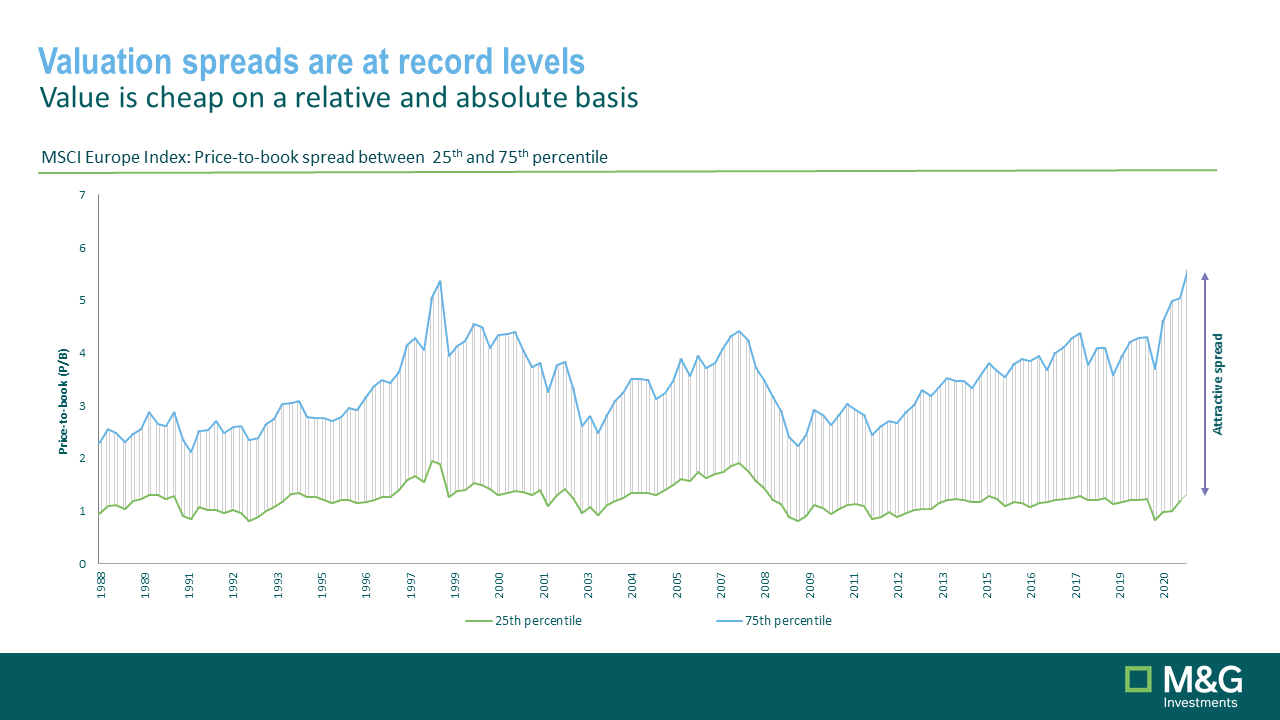

In contrast, despite the sudden and violent rotation into value, the valuation gap between the most expensive and the cheapest parts of the market has never been larger. As the chart below shows, the gap between the top and bottom quartile price-to-book ratio is still at a multi-decade high.

[caption id="attachment_26907" align="aligncenter" width="1280"] Graph showing MSCI Europe Index: Price to book spread[/caption]

Graph showing MSCI Europe Index: Price to book spread[/caption]

Some might argue that the valuation spread is due to the earnings power of the top end of the market accelerating in a changing economic environment. This is, however, not the case. While the dispersion between the most expensive and the cheapest parts of the market has steadily grown since the Global Financial Crisis (GFC), this is due, predominately, to valuation re-rating at the expensive end of the market, and less to do with actual earnings growth. For us, this means there is plenty of room for further valuation compression from the expensive end of the market.

We believe the biggest driver for the ‘return of value’ lies in this unsustainable valuation dispersion. As the regime change gets underway, we are likely to see the source of growth change. Challenges to the sustainability of returns at the high end should cause extended valuations to retreat. While improved opportunities for return at the bottom end of the market should put upward pressure on valuations.

As we have seen in the past several month, the snap back is already happening. It is no longer a question of when. As one sell-side research house has pointed out, ‘value stocks are now becoming the new momentum stocks’. In a desert of high-yielding assets, value stocks could be one of the last oasis to provide investors with much needed returns.

While we are very positive on the return of the value style, we are also aware that there are many structural challenges in some of the typical value sectors. Even before COVID-19, we were seeing some very big changes in the global economic model. Now as we slowly come out of a global lock down, old and new challenges abound. In times like these, it is vital that investors remain nimble to avoid pitfalls and take advantage of new opportunities.

In the past few years, investors would have done well from simply investing in the largest companies in the US stock market. As this trend looks to be reversing, we believe now is a particularly good time for active managers to add value. Stock picking is a delicate art of balancing risk against valuation. This art, temporarily, lost its importance when the market was supported by strong themes of abnormal growth, prolonged low interest rates and economic transformation. Ultimately though, valuation and stock picking does matter.

Avoiding value traps

While we believe the cheapest quartile of the market is a rich hunting ground for good longer-term investment opportunities, we also recognise that there are many value traps. As more investors are looking at the style, we would caution against investing indiscriminately in cheap stocks. Stock picking in this environment is more important than ever.

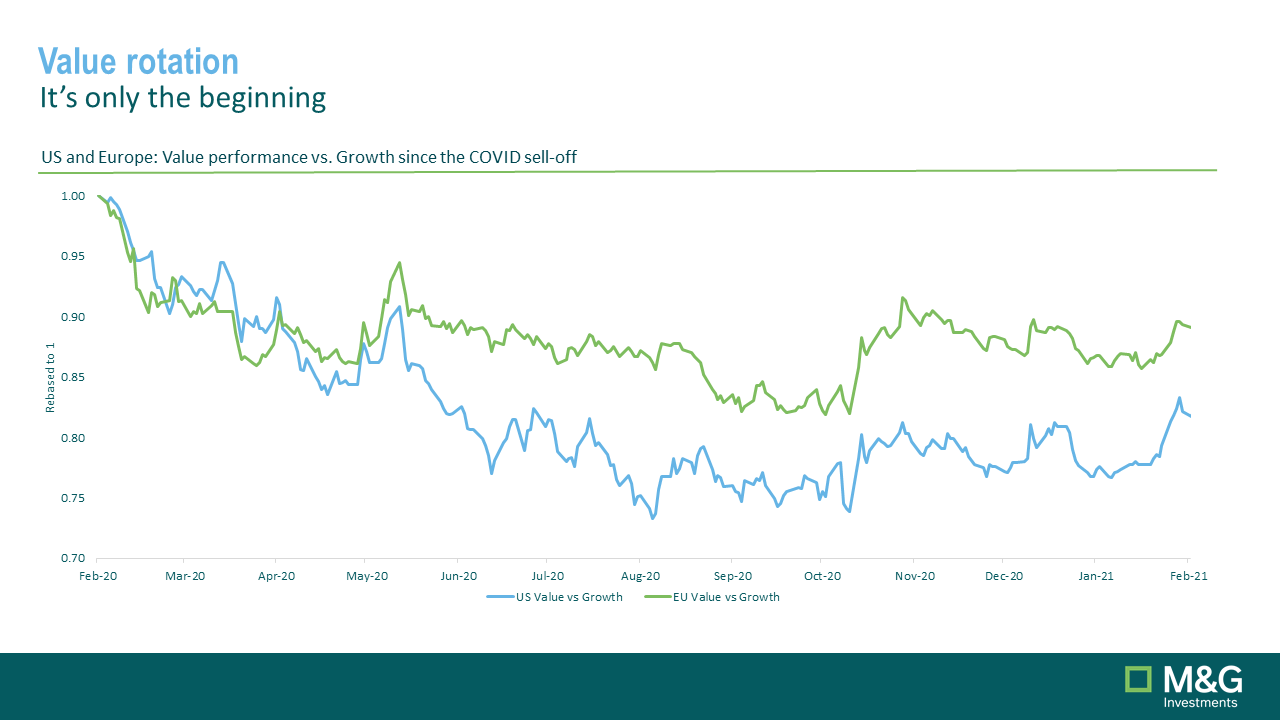

We believe the value rotation has only just begun. Despite recent recovery, value stocks have yet to recover to pre-COVID levels.

[caption id="attachment_26908" align="aligncenter" width="1280"] It's only the beginning: Value performers vs. Growth since the COVID sell-off[/caption]

It's only the beginning: Value performers vs. Growth since the COVID sell-off[/caption]

As mentioned above, the valuation dispersion between value and growth was already at historical highs prior to the pandemic and subsequent lockdowns. In our opinion, this rotation could be a once in a generation opportunity for investors, and indeed, could be the start of a trend for cheap assets that defines the current decade. With careful stock selection, the opportunity ahead is truly exciting.

About the author

Richard Halle, Fund Manager, M&G Investments

Richard graduated from the University of Natal in South Africa with a Bachelor of Commerce degree. He started his career as a securities analyst at Sedgwick Group and in 1999 he joined M&G as an investment analyst specialising in the insurance sector. Richard joined the European equities team in 2002 and became a fund manager in 2008. He is a Chartered Financial Analyst.

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on or treated as a substitute for specific advice of any kind.

We make no warranties, representations or undertakings about any of the content of this website; including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representations, warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Richard Halle, Fund Manager, M&G Investments

Richard graduated from the University of Natal in South Africa with a Bachelor of Commerce degree. He started his career as a securities analyst at Sedgwick Group and in 1999 he joined M&G as an investment analyst specialising in the insurance sector. Richard joined the European equities team in 2002 and became a fund manager in 2008. He is a Chartered Financial Analyst.

Read more articles by this authorBe the first to hear news and insights from Embark Group

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.