Are growth and inflation back and set to stay? Juan Valenzuela gives his view in this Q&A.

In the last few months, economic growth has picked up markedly. Do you expect this to continue?

If we consider the three main areas that drive the economy – households, corporates and the public sector – all look poised for a strong recovery.

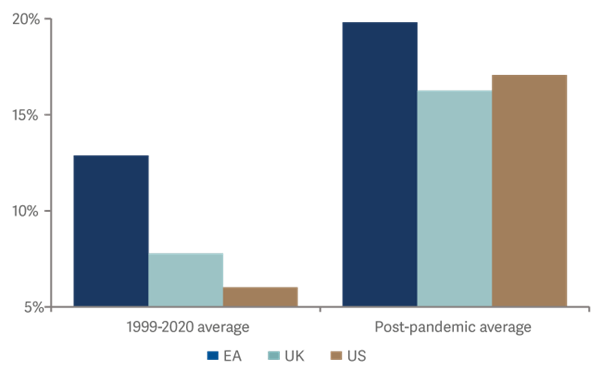

Taking private expenditure first, it’s hard to think of a moment in history when, just after a major recession, consumers’ balance sheets look much better than they did before it. But that is the case at the moment. There has been an unprecedented increase in savings, particularly in the US and the UK, as displayed by the below chart. In the US, this has been accompanied by a meaningful increase in disposable income, helped in part by the Democrats’ stimulus package of income support and tax credits.

Household savings rate

Source: Bloomberg as at 31 March 2021.

As well as saving more, consumer spending has been boosted by the ‘wealth effect’ because of rising asset prices. The housing market in developed markets is booming. Higher wealth supports confidence and this leads to more spending. In short, there is a substantial amount of potential demand ready to be released when economies reopen.

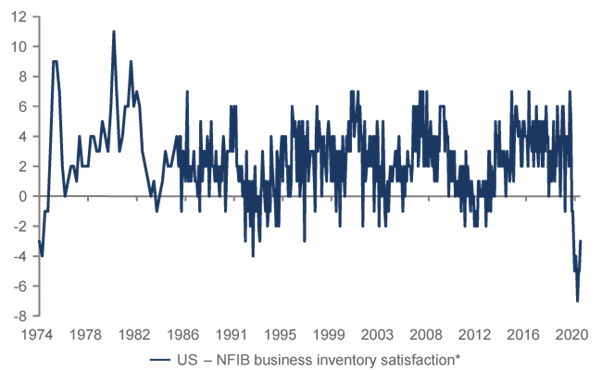

In the corporate sector, the level of inventories is inadequate to meet demand. The US small business survey, which has been running for about 40 years, shows that the level of inventory has rarely been lower (as displayed in the chart below). There is a high level of confidence that rebuilding inventories will boost growth.

Corporate sector - Depressed inventory levels will support future activity

Source: *Bloomberg, NFIB small business survey as at 31 March 2021

The recovery in global trade has been impressive. After the Global Financial Crisis, it took almost two years to get back to the same level. This time it has taken just six months.

Finally, in the public sector, governments will continue to run expansive fiscal policies this year and possibly next.

The prospects for all three sectors are pointing to higher growth in the near term – possibly much higher than expected.

What does this mean for inflation?

We are all aware that inflation, particularly in the US, has been increasing quite meaningfully. Without being complacent, we believe much of this is due to year-on-year base effects, particularly the change in energy prices from the trough in the spring of 2020. It is also related to the opening up of the service economy, which should translate into higher air fares and hotel prices. The unwinding of some of the tax cuts that were enacted in 2020 will also play a part. Over the course of this year, these factors will all be supporting inflation. But beyond the peak in 2021, we need to distinguish between higher inflation due to these base effects and more sustained increase in underlying inflation.

Many of the policies enacted last year will postpone the economic hit of the pandemic. In the UK, for example, there are still three million people on furlough. Thanks to government support, bankruptcies have actually gone down, in contrast to what we normally see in recessions. Unwinding these policies will be complex and the effect on growth is unpredictable.

Is higher economic growth a short-term phenomenon or sustainable over the longer term?

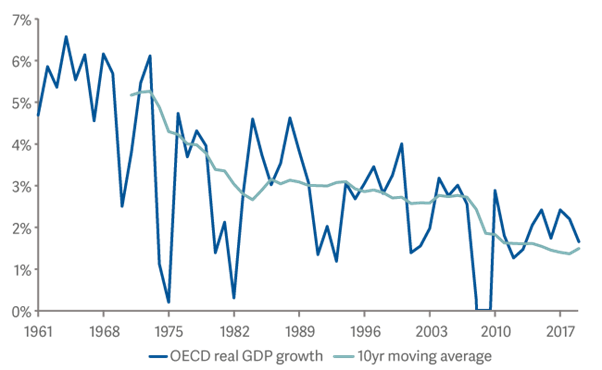

Simply extrapolating the current increase in growth and inflation into the future may be a mistake. We need to consider the structural dynamics that have been driving global growth lower for the last few decades. Crucially, the working-age population will reduce significantly, particularly in China. So unless we see a meaningful increase in productivity the negative trend in global growth as displayed in the below chart, is unlikely to change.

Global economic growth is structurally lower

Source: World Bank as at 31 December 2019

More generally, ageing populations are a major challenge. A great many people will retire over the next 10-15 years. These workers will be saving aggressively. In addition, the recent accumulation of public debt due to the pandemic will translate into higher taxation, focused on assets and wealth. This will further incentivise saving. So, we are very much in the middle of the ‘savings glut’. At some point, of course, the balance between savings and investment will change - but we don’t think we’re anywhere near that point.

If we compare inflation in the US over the last cycle with those of the previous 100 years we see that despite the increase in the monetary base, inflation has been quite subdued. Inflationary fears that we had with the onset of quantitative easing in 2009 have not materialised. This is in part because increasing money supply is offset by decreasing money velocity (money turnover) and so is not feeding through to higher prices.

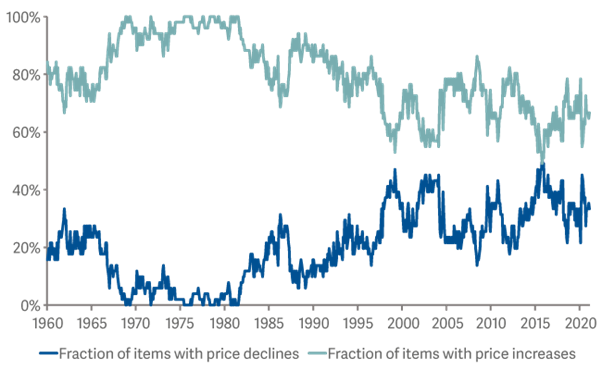

It's also interesting to look at price dispersion in the US (as displayed in the chart below). Items with price declines represent a larger proportion of total goods and have remained constant, suggesting that these items are beyond the control of domestic monetary policy.

US inflation - price dispersion

Items with price declines represent a larger population.

Source: Federal Reserve Bank of San Francisco as at 1 February 2021

Rather, they seem to be driven by global and technological trends. As a result, US inflation has undershot its target consistently over the last 10 years. The pandemic has accelerated some of the trends already in place. One example is the growth in online shopping, which is suppressing prices for a range of goods.

To conclude, in the near term we need to embrace the inflationary narrative. Growth and inflation are going to be higher and central banks are going to be worried about being behind the curve in tackling them. In the short term, inflationary risks will seem quite real. However, because of structural trends in place, extrapolating these risks into the long term might be a mistake.

For a more detailed look at what inflation could mean for markets please view Juan’s recent article Another look at inflation.

Important information

The intention of Artemis' 'investment insights' articles is to present objective news, information, data and guidance on finance topics drawn from a diverse collection of sources. Content is not intended to provide tax, legal, insurance or investment advice and should not be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any security or investment by Artemis or any third-party. Potential investors should consider the need for independent financial advice. Any research or analysis has been procured by Artemis for its own use and may be acted on in that connection. The contents of articles are based on sources of information believed to be reliable; however, save to the extent required by applicable law or regulations, no guarantee, warranty or representation is given as to its accuracy or completeness. Any forward-looking statements are based on Artemis’ current opinions, expectations and projections. Articles are provided to you only incidentally, and any opinions expressed are subject to change without notice. The source for all data is Artemis, unless stated otherwise. The value of an investment, and any income from it, can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested.

About the author

Juan Valenzeula, Fund Manager, Fixed Income Team, Artermis

Juan has degrees in both Law and Business from Carlos III University in Madrid. He began his career in 2003 at JP Morgan in Edinburgh. He joined SWIP in 2006 to manage several mandates, including its Absolute Return Bond Fund. Juan went next to Alliance Trust, where from 2012 he helped launch and then co-managed the Dynamic Bond Fund. Before joining Artemis in February 2019, Juan worked from 2015 at Kames Capital, where he co-managed Kames’ Strategic (onshore and global) Bond Funds, LBPAM Kames Absolute Return Bond Fund and Core Plus Fund. Juan is a CFA charterholder.

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on or treated as a substitute for specific advice of any kind.

We make no warranties, representations or undertakings about any of the content of this website; including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representations, warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Juan Valenzeula, Fund Manager, Fixed Income Team, Artermis

Juan has degrees in both Law and Business from Carlos III University in Madrid. He began his career in 2003 at JP Morgan in Edinburgh. He joined SWIP in 2006 to manage several mandates, including its Absolute Return Bond Fund. Juan went next to Alliance Trust, where from 2012 he helped launch and then co-managed the Dynamic Bond Fund. Before joining Artemis in February 2019, Juan worked from 2015 at Kames Capital, where he co-managed Kames’ Strategic (onshore and global) Bond Funds, LBPAM Kames Absolute Return Bond Fund and Core Plus Fund. Juan is a CFA charterholder.

Read more articles by this author

Be the first to hear news and insights from Embark Group

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.