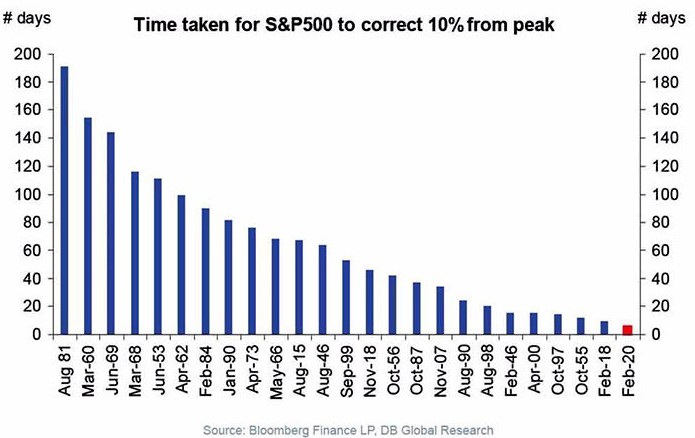

Two weeks ago, the S&P 500 Index fell 11.4% in a single week. What is the precedent for a move of this magnitude? Since 1926, there have been only 15 other further instances where the US benchmark was down 10% or more from Friday close to Friday close. In modern times this market decline by 10%+ counts as the fastest ever.

History shows that falls of such speed and scale offer little by way of a pattern as to “what happens next”. In the great depression of the 1930s markets fell further but in many other cases markets went on to perform strongly. The scenario with COVID-19 seems to be quite unique.

In terms of the developed market economies nothing seems to be broken, unlike the 2008 Global Financial Crisis where the banking industry had become poisoned. In the current scenario the impact is with human infrastructure and an economic model built on global trade and a shock impact to a manufacturer’s essential security of supply.

The current sell-off suggests investors are pricing for a U-shaped recovery. In other words, not a single quarter impact to earnings but something longer, deeper and uglier altogether. Today’s Fed rate cut of a substantial 50bps rather added fuel to this scenario. This is almost certainly not what the Fed intended but is how markets have initially read the move.

Amongst others, Goldman Sachs have modelled the impact on earnings as a steep one quarter decline and a sharp upward revision thereafter - the real impact effectively being spread across two quarters. The OECD have downgraded 2020 global growth from 2.9% to 2.4%. So, not a global recession but a marked slowdown courtesy of COVID-19. News from China suggests workers are returning to factories, motivated by local party officials whilst numbers of new infections and deaths continues to fall. Across developed markets we are around 6-8 weeks behind China, so early stage impacts are broadly unknown. This is the fear that drives markets lower. Self-isolation requires a discipline that is not immediately obvious in the West and may of course be difficult to enforce.

Health care stocks and business services providers of remote communication software will be in very strong demand from workers able to operate efficiently from home. It could be the incidence of COVID-19 brings a change in economic and manufacturing philosophy. The process of offshoring could well be reversed, with manufacturers and politicians alike embracing onshoring and/or nearshoring. This would certainly fit President Trump’s “America First” mantra.

The outbreak of COVID-19 will only become a long-term and more substantial issue if the gravity and subsequent lock-down that follows is even longer than anticipated. A short-term shock to earnings, whilst unpleasant and unplanned, is not the end of the world. The real danger for markets lies in a much more prolonged impact where businesses suffer acute cash-flow problems with the knock-on impact to banks who experience non-performing loans and then we ultimately end up with another banking crisis. This is a long way off but is something we should monitor.

With warmer weather approaching in April and May plus the expectation that central banks will expand balance sheets further and do “whatever it takes” we are more confident the worst of the economic impacts can be held at bay. Of course, a vaccine or successful treatment available on a mass scale is the real silver bullet.

Asim Javed, Senior Investment Manager, Alpha Beta Partners

Asim is a highly qualified Senior Investment Manager and Risk Manager. He is a Chartered Financial Analyst (CFA) charter holder and a Chartered Accountant with over ten years investment management and portfolio oversight experience.

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on treated as a substitute for specific advice of any kind.

We make no warranties, representatives or undertakings about any of the content of this website (including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representation warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Asim Javed, Alpha Beta Partners

Asim is a highly qualified Senior Investment Manager and Risk Manager. He is a Chartered Financial Analyst (CFA) charter holder and a Chartered Accountant with over ten years investment management and portfolio oversight experience.

Read more articles by this author

Be the first to hear news and insights from Embark Group

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.