The spring and early summer 2020 has been a period of superlatives in investment markets. Covid-19 has brought in its wake the fastest global falls in stock market history and one of the fastest rebounds in equity values – thanks to central bank activity.

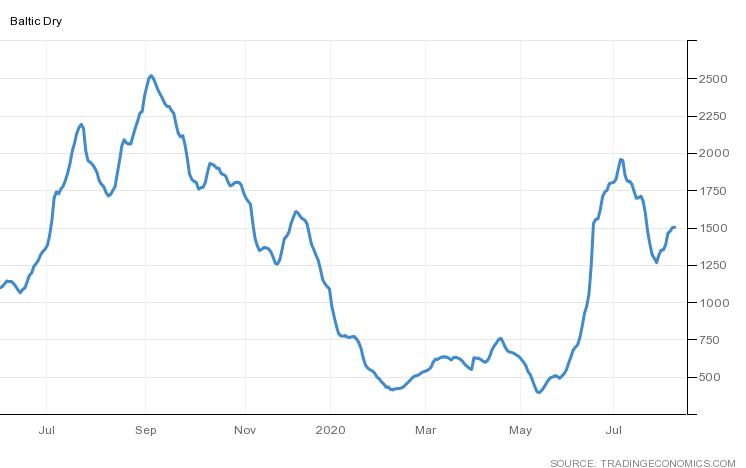

We saw unprecedented rises in unemployment, particularly in the United States, and hugely expensive furlough schemes paying workers to stay at home. Oil prices fell to the lowest on record in April when the price of crude oil for May delivery traded as low as -$16.74 a barrel. Other commodity prices collapsed based on the lockdown in global trade. The Baltic Dry Index is reported daily by the Baltic Exchange in London and was, like other indicators, heavily impacted. The index provides a benchmark for the price of moving major raw materials by sea. The index considers 23 different global shipping routes carrying coal, iron ore, grains and oil, and is considered a good barometer for global trade in essential commodities. Central banks stepped in to provide huge injections to capital markets which had a desired impact of arresting the collapse in values and provided a powerful catalyst to reboot an economic recovery – in many ways a major dose of adrenalin has been injected to markets. A broad array of leading economic indicators began to rebound positively in value.

The chart shows the troughing and subsequent rebound in the Baltic Dry Index.

The rally in share prices around the world has been encouraging but the leadership of the fight back and surge into the area of new highs has been the preserve of technology giants such as Facebook, Amazon, Netflix and Microsoft – all businesses which have found even greater demand in a lockdown environment. Mr Elon Musk’s electric car maker, Tesla, soared to new heights and is now valued more than the likes of Toyota, BMW and Volkswagen. Elon Musks’s personal fortune boosted by his other successful business, Space-X, skyrocketed in excess of $35bn, eclipsing stalwarts such as Warren Buffet.

Once again investment fundamentals have moved into overvalued territory with various indicators suggesting share prices are fully valued as earnings fall away based on disrupted demand dynamics courtesy of Covid-19. Whilst technology firms have broadly enjoyed enhanced demand, their valuations are tricky to justify at these elevated levels. A slip-up in performance is likely to see a correction in share prices of even the biggest technology leaders. Markets are clearly looking through the current economic hiatus and out to the other side when normal service can be resumed.

Any disruption to this philosophy or its associated timeframe will bring market volatility. This is clearly what we have witnessed over recent weeks with so called “smart lockdowns” put in place in certain US states and in areas of the UK and Europe. Our forecast earlier this year of what we called a corrugated recovery has certainly proved to be correct. Last week the IMF set out a very wide range of possible recovery paths underlining the risks that still exist.

Markets have maintained their love affair with high-growth businesses, leaving more traditional, so-called value stocks out of favour, despite in many cases having far more appealing valuations.

We know financial repression, the economic strategy used to combat the effects of the Great Financial Crisis in 2008-9, tends to inflate the value of risk assets over time. This has broadly been good for investors in most asset classes other than cash. The economic response to the pandemic is financial repression in the guise of mind-boggling quantities of quantitative easing, asset purchases and yield curve manipulation. The sheer size of the response so far has brought Modern Monetary Theory (MMT) into play. MMT is a form of accelerated financial repression, one that allows central banks to print huge sums of money to deliver a range of economic stimuli such as infrastructure development and renewal. Commentators are referring to this as the 21st century “new deal” set to rival that of FDR Roosevelt in the late 1940s and 50s, which led to the American golden age. Modern businesses, digitisation, health and wealth-related adaptations and innovations, as well as the more obvious infrastructure renewal and low-carbon industries, are perhaps amongst the biggest winners.

Ballooning debt-to-GDP ratios will become the norm as has been seen in Japan over the past decade. Government debts can be serviced whilst interest rates remain low and this is likely to be the case for the foreseeable future. Inflation is of course the risk, which could help to reduce the real level of debt over time but will also have a damaging impact upon economies and their currency values. The US dollar’s preeminent position as the go-to global currency of choice remains an important feature when considering the possible downsides associated with MMT. Gold has rallied very significantly, largely due to investors seeking an asset class which could store value in the event that economic policies do not go well. Alpha Beta portfolios have benefitted from our allocation to the precious metal.

The chart shows the strong recovery and new highs for the technology-rich NASDAQ index.

At a geopolitical level, the stakes are rising with potential to impact markets later this year and into 2021. The US Presidential election is of global importance. The political and economic differences between Messrs Trump and Biden could not be starker. Despite undeniable style idiosyncrasies, markets would prefer Mr Trump being returned to the White House. His political opponent, with his interventionist and higher-tax proposals, could disrupt a rally in markets. We anticipate volatility rising as we approach the election in November. We will consider the prospects later this year as we move into autumn and the potential to take some risk from portfolios will be reviewed. The economic cold war that is developing between China and the United States and her allies is important to monitor. We have moved beyond a trade war with the imposition of tariffs to a policy of starving China of dollar investment. We remain underweight emerging markets despite a fall in dollar strength.

In Europe Mrs Lagarde, Head of the ECB, and Mrs von der Leyen at the European Commission are making bold strides to tackle the economic damage inflicted by Coronavirus. A €750 billion package will be presented to EU member states for sign-off. European equities have performed strongly in recent weeks – again, Alpha Beta portfolios benefitted from an increased allocation to the region in recent times. In Great Britain markets have been held back by Brexit fears and a heavy mix of oil stocks and miners in our major index. At a lower level, valuations are appealing, and a move upwards has been apparent of late.

At a technical level we have seen equity markets range bound for some time in the past several weeks, with the S&P 500 struggling to break the 3300 mark. A possible rotation from the narrow leadership of the handful of technology behemoths to a broader base of diversified industries is possibly underway and this could be the catalyst the market needs to move forwards. The 5-year UK Gilt yield has fallen into negative territory. The 10-year Treasury yield has now fallen to meet the swap-rate curve (a predictor of yield curve definition), again as we forecast, and we cannot envisage significantly more yield compression in investment grade credit unless a negative interest rate policy is adopted anytime soon.

Overall, we view opportunities in markets positively and believe risk assets are well supported over the medium to longer term.

For more insights articles such as this, please visit our insights page

About the author

Asim Javed, CFA, Senior Investment Manager

Asim is a highly qualified Senior Investment Manager and Risk Manager. He is a Chartered Financial Analyst (CFA) charter holder and a Chartered Accountant with over ten years’ investment management and portfolio oversight experience.

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on treated as a substitute for specific advice of any kind.

We make no warranties, representatives or undertakings about any of the content of this website (including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representation warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Asim Javed, Alpha Beta Partners

Asim is a highly qualified Senior Investment Manager and Risk Manager. He is a Chartered Financial Analyst (CFA) charter holder and a Chartered Accountant with over ten years investment management and portfolio oversight experience.

Read more articles by this author

Be the first to hear news and insights from Embark Group

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.