2020 has certainly offered some unique challenges for those whose day job it is to try and assess markets in the Covid-19 netherworld in which we find ourselves.

We witnessed one of the sharpest bear markets ever in February and March, provoking massive and coordinated central bank intervention, led by the US Federal Reserve. This added much-needed liquidity to markets and put a floor under the falling prices of risk assets. The subsequent rally from the March lows has been equally ferocious, with the US tech giants in the vanguard. Thus far, it has been a win-win for the so-called disrupters and internet platforms on both sides of this crisis.

As we enter the final quarter and ponder where we are now, and where we might be heading, it is instructive to compare 2020 with two other famously difficult years, 2008 and 2000. Indeed, coronavirus or not, many of the fundamentals are strikingly similar.

Y2K – the first mania

If we look at the situation in 1999 ahead of the Dot-Com crash in 2000, the Federal Reserve (and other central banks) had been cutting interest rates aggressively and providing ample liquidity in advance of potential Y2K issues. At the same time, economic growth was deteriorating.

From a stock market perspective, a clear warning sign was that aggregate equity valuations were exceeding the extremes seen in 1929 and earnings were not actually growing. Margin debt was at an all-time high and investor sentiment was very bullish. New metrics were being created to value companies, the IPO market was red-hot and if you didn’t own Dot-Com stocks, you felt as if you weren’t in the game.

The GFC

Fast forward by just under a decade to 2008 and the Federal Reserve was flooding the market with liquidity to stave off the growing sub-prime crisis, with other central banks in a similar easing mode. Interest rates were falling rapidly.

Leverage and debt were feeding a property frenzy, creating another false wealth effect, while share buybacks were rampant. Once again, margin debt was rising rapidly, reflecting the enthusiasm to own stocks.

The stock market had been moving up seemingly exponentially and another term, ‘the Goldilocks economy’, was created and popularised which meant no one could lose – until, of course, they did.

The IPO market was again bubbly and if you didn’t own real estate, you supposedly weren’t in the game.

Work from home mania

Turning to 2020, the Federal Reserve and other central banks are again flooding the market with liquidity to stave off the global economic slump caused by the pandemic and to fund the measures to fight it.

Interest rates are falling rapidly. Like 2000 and 2008, earnings barely grew last year and are now fading fast. Share buybacks were rampant in 2019 and into 2020. Margin debt was moving sharply higher into the crash of early 2020.

The ‘stay-at-home’ stocks are the new speculative bubble and the IPO market is red-hot too.

The valuation perspective

At times like this, it is vital to ground expectations about the prospects for returns against a sense of valuations today. Below, we highlight a couple of market metrics that provide a sense of the valuation backdrop for US equities, which, by most valuation measures, are richly priced.

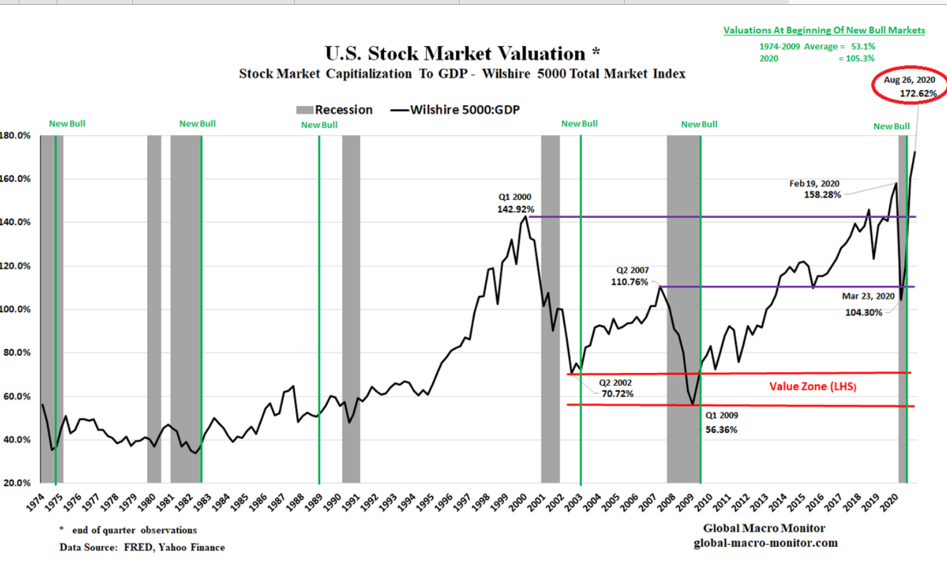

The first is Warren Buffet’s favourite, namely, the ratio of the market cap of the Wilshire 5000 Total Market Index to US GDP. This metric reached a record-breaking 158% in 2019 and has risen further to 172% as of late August 2020.

In short, if there was cause for caution in 2019, then there are even greater grounds for caution now.

The second metric, a measure of the S&P 500 Forward P/E, is shown below. It stands at over 26x, just shy of its tech boom high, which was its previous all-time peak.

Beware the heroes

Every bull market has its hero stocks, but it is interesting just how many are trading at remarkable valuation ratios at the current time. For example, Moderna, the US biotechnology company, is on a stratospheric price to sales ratio of 241x. Were it to produce the first and successful vaccine to combat Covid-19, perhaps that ratio would be justified but a great deal of optimism is baked into its stock price. Another example is Zoom; it has risen to 68x price to sales as it has found itself at the heart of the ‘stay-at-home’ dynamic. Many other ‘hot’ stocks are at similarly heady levels and the question for investors is whether these businesses justify these levels of optimism. We would argue that many of the momentum-fuelled, ‘stay-at-home’/vaccine stocks represent another speculative bubble and therefore, investors need to be alive to this risk and trade them accordingly.

The so-called “FAANGs” are another source of contentious debate, although here, it is difficult to argue that the tech giants are not well placed to weather, and indeed benefit from, further market disruption. They have significant cash resources, provide solutions to remote working and the digital economy and operate in markets that can be served relatively safely, even in the midst of lockdowns globally. Dominant or near-dominant positions, and the expectation that their power base stands to grow, supports the narrative. In fact, we would argue that it is competition laws rather than valuations that pose the biggest threat to the big-cap tech beasts.

There is value elsewhere

It is worth noting that while those stock markets that do not feature large technology constituents have rebounded, they have lagged meaningfully. The FTSE 100 is notable in this regard, being heavily weighted in companies in the energy, mining and financial sectors that rely on a broader global economic recovery and a normal (or nearer-normal) interest rate environment. Equally, while emerging markets cannot escape the effects of the global economic downturn, they have relative valuation on their side and thus far, the Asian region has had more success in containing the Covid-19 virus. Indeed, value investors across all markets are finding opportunities in many sectors and stocks but until we reset the normal workings of global economic activity, a switch away from the flavour of the day seems a distant hope, despite the very obvious value on offer.

Conclusion

This analysis has been a brief run through some of the issues that we debate with fund managers on a daily basis. The world is always uncertain, but at the present time, the sense of uncertainty is at an extremely elevated level. We have demonstrated that certain assets and markets are overheating and we remain cautious about risk assets on a near-term basis.

However, opportunities are already emerging for the patient investor – the world never stops, and normality will return. For now, stay diversified and anticipate more buying opportunities as we move into next year. The best investment tip is one of the oldest: be brave when others are fearful but also remain patient.

2020 may still have a few more stories to tell yet.

For more articles, please visit our insights page

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on treated as a substitute for specific advice of any kind.

We make no warranties, representatives or undertakings about any of the content of this website (including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representation warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Peter Toogood, CIO, Embark Group

Peter launched The Adviser Centre in May 2014, whilst employed by City Financial He was co-founder of the original Forsyth-OBSR Ratings Service in 2002. He joined OBSR in 2008 and was responsible for establishing the firm’s fund advisory business as well as continuing to conduct manager research.

Read more articles by this author

Be the first to hear news and insights from Embark Group

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.