“How much can I withdraw from my pension portfolio, to avoid the risk of running out?”

Nobel Prize winner William F. Sharpe called this the single “nastiest, hardest problem in finance”.

Sharpe knows his onions – he is the 86-year-old retired professor of finance from Stanford University, 1990 Nobel Prize winner in Economic Sciences and has the Sharpe Ratio named after him.

New science

Not knowing future investment returns and the order in which they come, otherwise known as sequence risk, is the first part of Sharpe’s problem.

Since he considered the withdrawal question, however, a way of calculating the danger of sequence risk from any given asset allocation or portfolio has been developed.

With this new bit of science, withdrawal amounts can be accurately calculated by simply dividing the expected total return of a particular asset allocation by this new sequence risk term. The greater the value of this sequence risk term, then the lower the amount that can safely be withdrawn each year.

The second part of the problem is not knowing how long you will live, otherwise known as longevity risk.

This can be solved by establishing a planning horizon, for example 20 years, taking a retiree from age 65 to age 85. At the end of the planning horizon, the retiree may then convert a pre-determined residual amount left in a pension pot into a delayed annuity, providing income for the rest of their life, no matter how long that may be.

All that remains for the retiree is to consider the degree to which they can accept the risk of having to take a lower amount of annual income in future years to keep on track for that end point.

Some may not be able to accept less in the future while others may be less concerned and opt to withdraw at rate associated with say a 50% risk of shortfall. They would do this knowing that half the time they would be able to withdraw more in future years and half the time they are able to accept a future reduction, which would probably be not by very much.

Selecting an investment strategy for decumulation

Selecting the right investment portfolio is also key to a successful retirement.

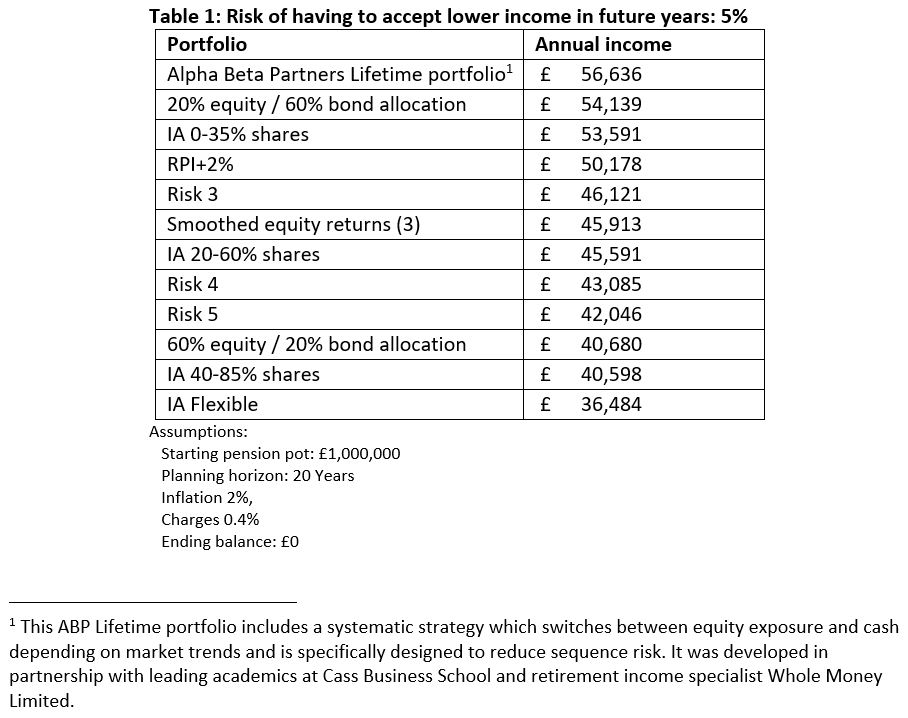

Table 1 shows the variation in sustainable withdrawal amounts attributable to various popular investment options.

As would be expected, the higher the equity allocation the greater the likelihood of suffering sequence risk leading to a higher sequence risk term and so the sustainable withdrawal amount is lower.

The difference between the highest and lowest sustainable withdrawal amount is as much as £20,000 in this example depending on the investment strategy selected, a very considerable difference.

Number of years of the planning horizon

The length of the planning horizon will depend on personal circumstances and can be changed at any time as situations change but is required to calculate the annual withdrawal amount.

As annuity rates rise in later life and personal ambition to remain in income drawdown may lessen, it will make sense for many to convert their pension pot balance into a delayed - and possibly enhanced - annuity.

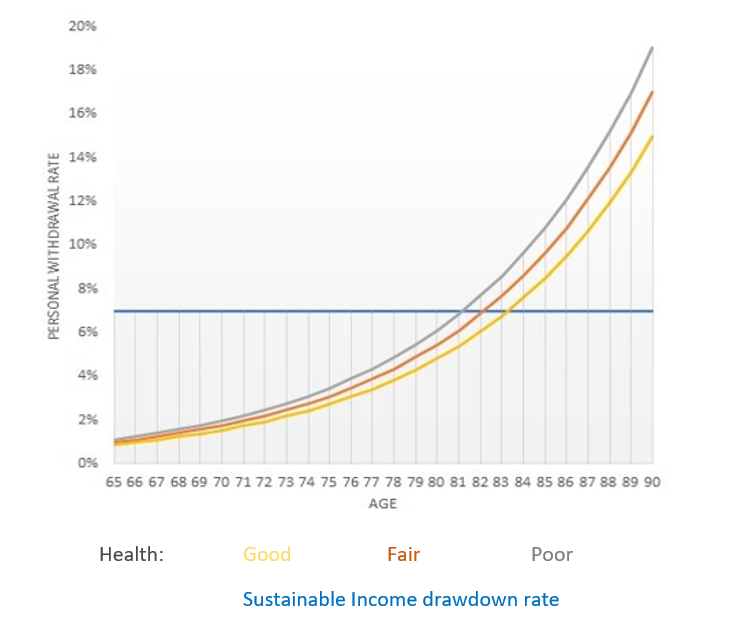

Graph 1 illustrates how and when annuity income outpaces drawdown income in later life. This form of analysis can be used to determine the potential length of the planning horizon and to support the decision as to when to buy an annuity.

Pulling it all together

There is no longer any need to approach income drawdown planning with ‘rules of thumb’ and guestimates.

The entire process has now been made scientific, from comparing and selecting investment portfolio types, calculating annual withdrawal rates and solving for longevity risk.

For more articles like this, please visit our insights page

About the author

Geoff Brooks, CEO, Alpha Beta Partners

Geoff has over 30 years’ experience in strategic and leadership roles in major financial institutions in Europe, Asia and the USA; Geoff developed his career as a retirement and investment expert advising and developing drawdown and retirement solutions. His early career started with 4 major life companies NPI, Standard Life, Prudential and Friends Provident. Later to be appointed Head of Retirement for HSBC launching Stakeholder Pensions, DC solutions and drawdown. At the forefront of consumer rights and value for money Geoff led the HSBC customers to contract back into SERPS as the first Life company to do so.

In 2006 a move to US as a senior vice president to lead the successful transformation of the HSBC Wealth business to a retirement and fee-based model and the re launch of Premier banking. This model having been translated to the global best practice, he was appointed to Global Head of Life pensions and Investments. Geoff delivered global growth and value for money initiatives with responsibility for the $2Bn profit enterprise. Having concluded his career with HSBC as CEO Offshore Insurance Europe in Malta Geoff is now playing a leading role in Alpha Beta Partners, a disruptive asset manager bringing retirement expertise and championing value for money and consumer outcomes.

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on treated as a substitute for specific advice of any kind.

We make no warranties, representatives or undertakings about any of the content of this website (including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representation warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Geoff Brooks, CEO, Alpha Beta Partners

Geoff has over 30 years' experience in strategic and leadership roles in major financial institutions in Europe, Asia and the USA; Geoff developed his career as a retirement and investment expert advising and developing drawdown and retirement solutions. His early career started with four major life companies NPI, Standard Life, Prudential and Friends Provident. At the forefront of consumer rights and value for money, Geoff led the HSBC customers to contract back into SERPS as the first Life company to do so. Geoff is now playing a leading role in Alpha Beta Partners, a disruptive asset manager bringing retirement expertise and championing value for money and consumer outcomes.

Read more articles by this author

Be the first to hear news and insights from Embark Group

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.