We are all aware that Covid-19 has had a massive impact on businesses around the country; businesses have lost large portions of their income which will clearly have a negative effect on liquidity.

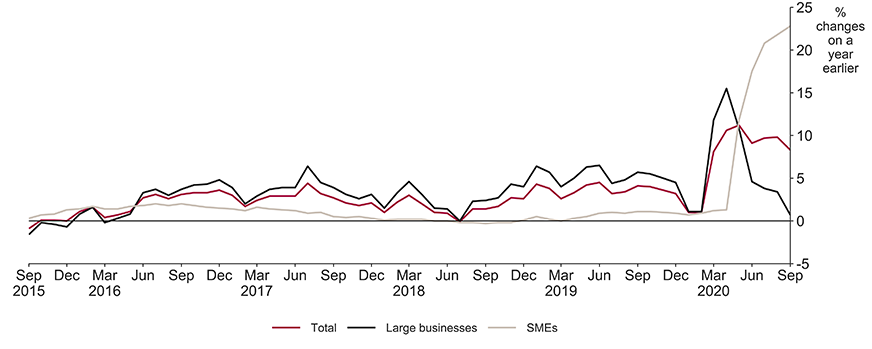

Small and medium-sized non-financial businesses continued to borrow from banks. In September, they drew down an extra £1.6 billion in loans (on net) and on average, net lending was £11.3 billion between May and July. These strong flows meant that the amount borrowed compared to last year had risen sharply since the start of the Covid-19 pandemic, growing to 22.8% in September, the strongest on record.

[Source: The BoE Money & Credit release Sept 2020]

In addition to this, the big five high-street banks — Barclays, HSBC, Lloyds, NatWest and Santander — have accounted for about 90 per cent of Bounce Back Loans so far. However, they are not taking on new customers. They complain about being inundated by demand from struggling small businesses for loans of up to £50,000, which are interest free for a year and are fully guaranteed by government.

All-Party Parliamentary Group on Fair Business Banking research has suggested that up to 250,000 small businesses “are effectively locked out of the market”, given they do not bank with accredited lenders [smallbusiness.co.uk].

If you have clients in this scenario, how would you advise your client to move forward? Instead of going to a commercial lender for further lines of credit or trying to arrange new or additional bank borrowing, there is an alternative.

Would the sale of company owned property to pension ownership provide valuable liquidity?

For over 40 years people have utilised the flexible investment options available within a SIPP and SSAS to benefit their own Ltd company.

The sale of property to pension is a common business planning topic, linked to a business needing liquidity. A business is often sitting on an asset such as property, which could be sold to their own pension therefore moving cash from the pension into the company. As we all know, pension schemes can only purchase commercial property, but this does vary from offices to industrial units. Not only does the sale of a commercial property to your client’s pension solve their initial liquidity issues, but it also drives tax efficiencies along the way.

When commercial property is held within a pension it is exempt from Capital Gains Tax, it will fall outside of the client's estate for Inheritance Tax and (if their company continues to operate from the property) the regular rental payments from the business are an allowable expense and will reduce their Corporation Tax liability.

If you like the idea but know your client's pension is not sufficient enough to purchase the property outright, there is the option of the pension borrowing up to 50% of the net assets from a commercial lender to assist with any purchase. Alternatively, their pension could part purchase some of the property with a view to purchasing the remaining share once it builds up sufficient funds.

Could a company use a cash injection courtesy of their pension scheme?

Another route to explore is via a SSAS loanback. The benefit of using a SSAS to assist with finance is that the client is in control of setting the interest rate. This flexibility is not possible from a commercial lender and allows the client to tailor the loanback to suit the company’s financial circumstances. Set it low to ensure you do not over burden the company with repayments - or - set it at the highest deemed commercially acceptable rate, which could give you an investment offering 7% or 8% return for 5 years.

The interest payments on a SSAS loanback are classed as a business expense in the same way as if the interest payments were paid to a bank, meaning that it can be offset against Corporation Tax. Increasing relief if interest payments are high, will in turn benefit SSAS funds which are within an IHT-free wrapper.

In order to satisfy HMRC requirements for a SSAS loanback, the scheme will need to take a first charge over a suitable asset. Other requirements also need to be met which are:

- The maximum loan being 50% of the net assets of the SSAS

- Max term of 5 years

- Regular capital and interest repayments must be made

- Interest needs to be a minimum of 1% above bank base rate

Looking at the current strong demand for liquidity in the SME market, the question that arises is whether clients can be in control of the uncontrollable (rates, source of funding). Taking this uncertainty out of the equation will potentially be a significant benefit to your clients.

Both options are great examples of how a client can utilise their pension fund to assist their Ltd company and also drive tax efficiencies. They also require in depth consideration for both the client and adviser which is where the ongoing support from your pension specialist is imperative.

For more articles like this, please visit our insights page.

About the author

James Cannon, Regional Sales Director, Embark Pensions

James joined the Embark Group in 2018, having spent over 15 years in the industry with other SIPP and SSAS providers Talbot and Muir, Xafinity and AJ Bell.

James specialises in providing dedicated support, technical expertise and a deep knowledge of self-directed pensions to Financial Advisers, Trustees and professional partners. He is focused on developing strong relationships within network of professionals who value high service standards and robust, prudent retirement provision.

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on treated as a substitute for specific advice of any kind.

We make no warranties, representatives or undertakings about any of the content of this website (including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representation warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By James Cannon, Regional Sales Director, Embark Pensions

James joined the Embark Group in 2018, having spent over 15 years in the industry with other SIPP and SSAS providers Talbot and Muir, Xafinity and AJ Bell. James specialises in providing dedicated support, technical expertise and a deep knowledge of self-directed pensions to Financial Advisers, Trustees and professional partners. He is focused on developing strong relationships within network of professionals who value high service standards and robust, prudent retirement provision.

Read more articles by this author

Be the first to hear news and insights from Embark Group

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.