"Decumulation strategies are still in their infancy. There is a danger that accumulation carries on into decumulation. I am not sure there has been enough thought put into a wide enough range of decumulation solutions." Sam Liddle, Church House Investment Management, October 2020.

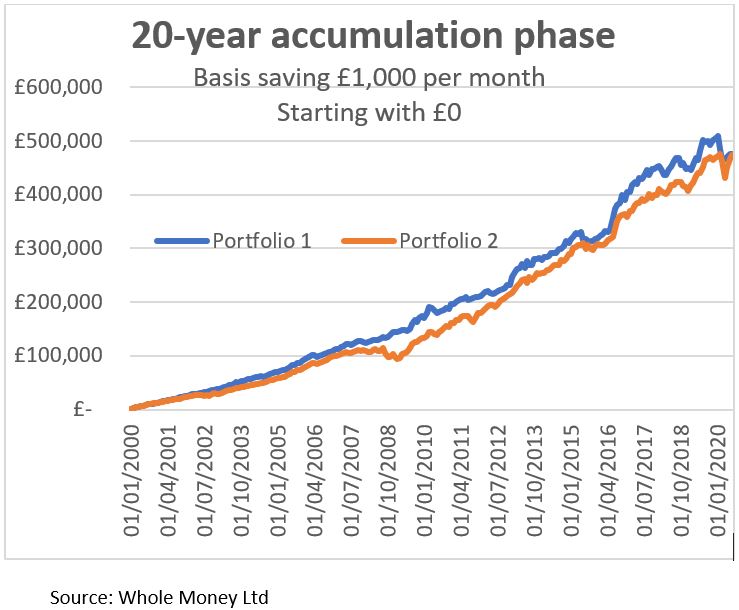

To illustrate the problem, consider the following example of two independently-constructed, mixed-asset growth portfolios. Both are widely available in the market today.

In the accumulation phase, £1,000 a month was invested into both portfolios for 20 years, starting on 1st January 2000 and ending 20 years later.

The investment outcome, when realised in 2020, was almost identical from both investments.

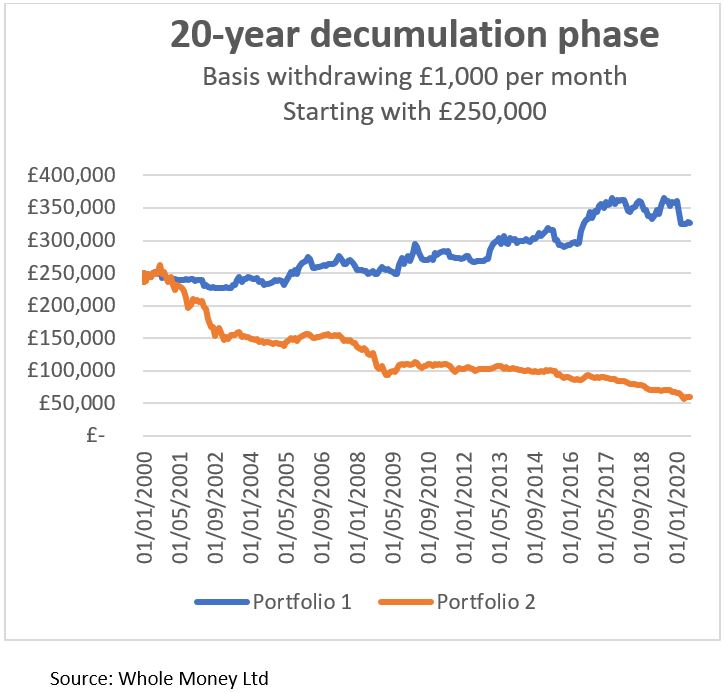

In the decumulation phase, £1,000 a month was withdrawn from the same two portfolios over the same period, but the outcomes were very different.

Sequence risk, the risk of suffering a series of poor annual returns while in decumulation, is the culprit.

Portfolio 2 suffered from the equity market losses associated with the dot-com bubble in 2001 and again from the great financial crisis of 2008. Due to capital depletion and the crystallisation of losses (from the need to withdraw funds annually), Portfolio 2 was never able to recover.

Portfolio 1 had a similar asset allocation but additionally included a strategy designed to mitigate sequence risk.

New developments

Renowned management thinker Peter Drucker is often quoted as saying that “you can't manage what you can't measure.”

Fortunately, academics recently developed a way to scientifically measure the sequence risk associated with any given asset allocation. Armed with this new metric, existing portfolios can be rated by the likelihood of their suffering from sequence risk, and new and better decumulation products can be developed.

Professors at Cass Business School have extensively researched the impact of sequence risk in decumulation and how it may be mitigated.

They have analysed target date funds, cash ‘buckets’, buying put option protection and varying allocations to stocks and bonds.

Their definitive conclusion after studying over 100 years of equity, fixed income and commodity price return data is that by switching systematically between equity exposure and cash, the worst instances of sequence can be mitigated, as displayed by Portfolio 2.

Risk in decumulation

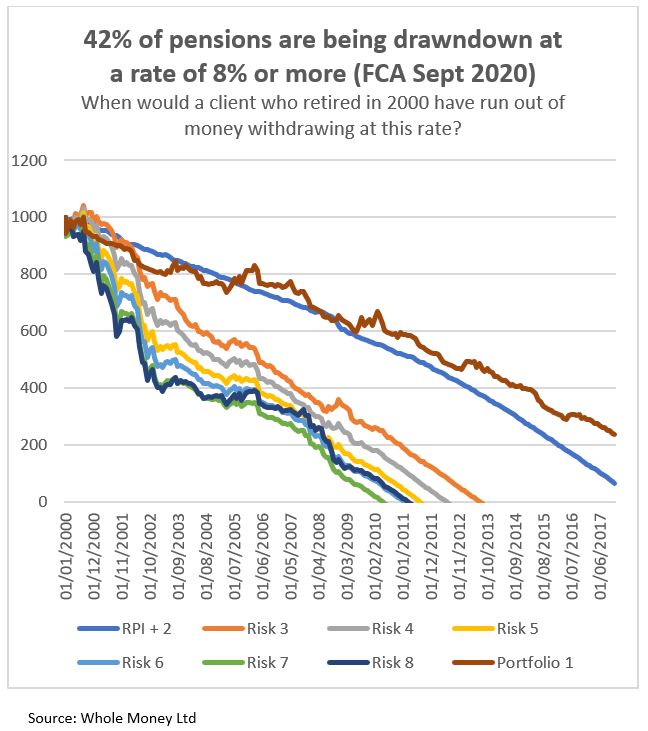

The requirement to ‘risk profile’ clients for their attitude to risk and their capacity for loss results in accumulation strategies being offered based on portfolio volatility. This approach has been naturally extended into decumulation, but volatility is only incidentally related to risk when in decumulation.

As shown below, the exhaustion dates of various volatility risk rated portfolios were not significantly different when drawn down at a rate of 8% starting in 2000. Only Portfolio 1 was still viable 17 years later.

The primary risk in decumulation is the risk of having to reduce withdrawals in the future to avoid exhausting a pension pot. This risk is directly related to the likelihood of, and the damage caused by, suffering large losses.

Let us consider how some promoted decumulation products have fared.

Lifestyle or Target Date Funds (TDFs)

A particularly unfortunate and highly publicised example of sequence risk in action occurred in October 2009 when the three biggest TDFs in the United States lost around 30% of their value one year prior to the 2010 target date. So serious was the impact, Congressional and SEC hearings were held.

Clearly, this was not supposed to happen given the funds’ de-risking approach. However, around the target date, these strategies still have around 50% exposure to equities, which once every 10 years or so can experience severe drawdowns of 40%–50%.

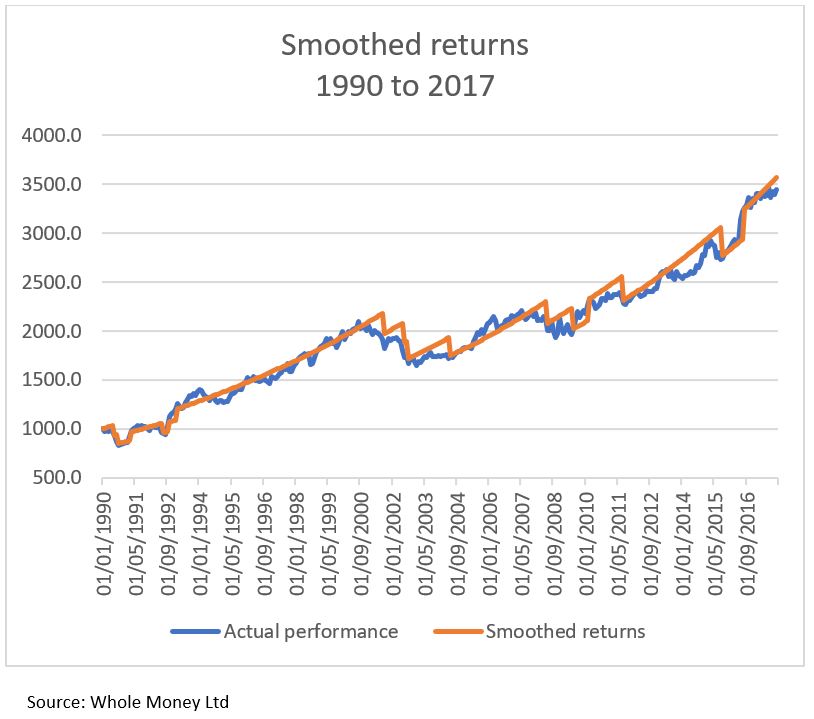

Smoothed equity returns

A popular drawdown investment has been into smooth managed funds and with profits type arrangements which aim to avoid sequence risk. The problem is that in practice they do not avoid sequence risk on most occasions and recently have offered sudden drawdowns of around 10% or more when the manager needs to realign the portfolio.

Actual fund data is not publicly available prior to 2008, however a robust simulation of performance since 1990 shows periods, in 2001 and 2008 particularly, when a series of 10% downward adjustments would have had to be applied. This would be to the significant detriment of retirees just nearing or entering drawdown when the value of their pension pots was greatest.

Each adviser will bring expert knowledge to help their clients navigate drawdown over what might be a 20 or 30-year planning horizon, and diversification is, as always, an important consideration.

Sequence risk can now be measured, and new and innovative portfolios specifically designed to mitigate sequence risk are now available. These will provide more options for advisers with which to construct a suitable drawdown portfolio and so improve retirement outcomes for their clients.

For more articles like this, visit our insights page

About the author

Geoff Brooks, Asset Manager, Alpha Beta Partners

Geoff has over 30 years’ experience in strategic and leadership roles in major financial institutions in Europe, Asia and the USA; Geoff developed his career as a retirement and investment expert advising and developing drawdown and retirement solutions. His early career started with four major life companies NPI, Standard Life, Prudential and Friends Provident. At the forefront of consumer rights and value for money, Geoff led the HSBC customers to contract back into SERPS as the first Life company to do so. Geoff is now playing a leading role in Alpha Beta Partners, a disruptive asset manager bringing retirement expertise and championing value for money and consumer outcomes.

For further information regarding this article please contact:

Andrew Thompson T: 07968 934127 E: [email protected]

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on treated as a substitute for specific advice of any kind.

We make no warranties, representatives or undertakings about any of the content of this website (including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representation warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Geoff Brooks, CEO, Alpha Beta Partners

Geoff has over 30 years' experience in strategic and leadership roles in major financial institutions in Europe, Asia and the USA; Geoff developed his career as a retirement and investment expert advising and developing drawdown and retirement solutions. His early career started with four major life companies NPI, Standard Life, Prudential and Friends Provident. At the forefront of consumer rights and value for money, Geoff led the HSBC customers to contract back into SERPS as the first Life company to do so. Geoff is now playing a leading role in Alpha Beta Partners, a disruptive asset manager bringing retirement expertise and championing value for money and consumer outcomes.

Read more articles by this author

Be the first to hear news and insights from Embark Group

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.